Onchain Credit Part 2

“Neither a borrower nor a lender be; For loan oft loses both itself and friend, And borrowing dulls the edge of husbandry.” — William Shakespeare, The Tragedy of Hamlet, Prince of Denmark, 1600

Part 2: So You Wanna Build a Lending Business?

Lenders do five things: 1) source capital from lenders and shareholders, 2) deploy capital by originating or buying loans, 3) collect interest and principal payments from borrowers, 4) liquidate collateral in case of default, and 5) do all of that while carefully managing duration and credit risk. Since at least the times of Shakespeare, lending has been considered to be - in contemporary language - a shitty business. Today’s essay discusses the underlying business physics of lending and the impact of tokenization.

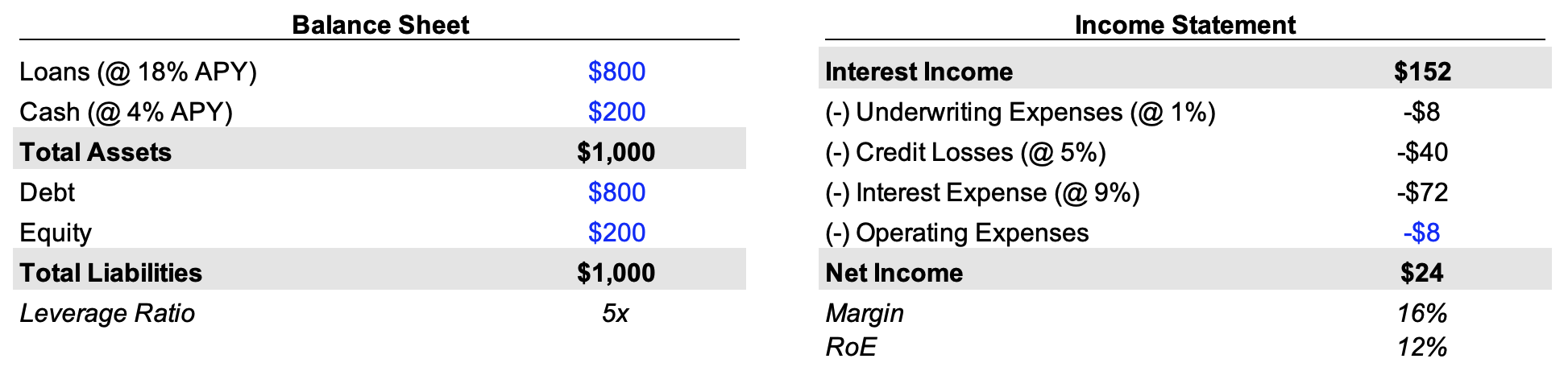

Let’s say you start a lending business tomorrow. You raise $200 of equity from your neighbors and get an $800 bank loan at a 9% rate. You keep a $200 cash buffer and loan out the rest equally among 20 of your friends at an 18% rate for twelve months. You earn $152 in annual revenues, spend $8 in gas to deliver and pick up the money ($0.40 per loan), pay yourself an $8 salary, leaving $136. One of your friends ditches town without paying, so you only actually take home $96. After paying back the bank loan at yearend, you and your neighbors take home $24 dollars in total profits and earn a 12% return on equity.

Starting balance sheet and year-1 income statement for our illustrative lending business.

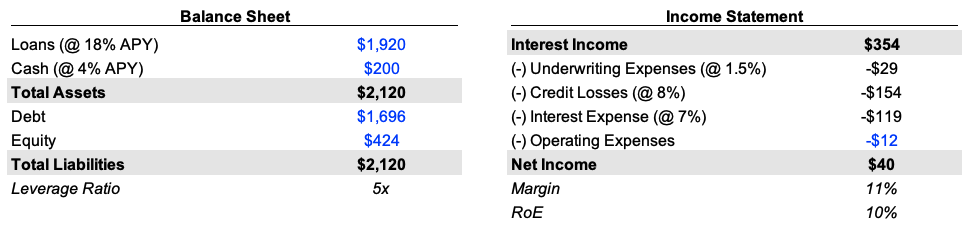

The next year rolls around and you’re ready to scale. You raise another $200 of equity capital and now have $424 of equity on the balance sheet, including last year’s profits. You go back to the bank to negotiate a bigger loan (+$1,700) and a reduced rate of 7% APR. You ask each of your friends for referrals, and each of them introduces you to a few (1.5) of their friends. You keep the $200 cash buffer and loan out the rest across 48 of your first- and second-degree friends at 18%. At first, things look great: you’ve more than doubled revenues from $152 to $354 and reduced your cost of debt from 9% to 7%.

As the year goes on, your assumptions face a tough reality. Your friends’ friends live further from you, which means you now spend $0.60 of gas driving to each of them. You don’t know them as well as your first-degree friends, so four of them end up ditching town without repaying. You hire a part-time assistant to manage the increased workload and pay them an extra half of your salary. Even with the lower interest rate charged by the bank, you end up generating only $40 of profits and delivering a 10% return on equity.

Year-1 starting balance sheet and year-2 income statement for our illustrative lending business.

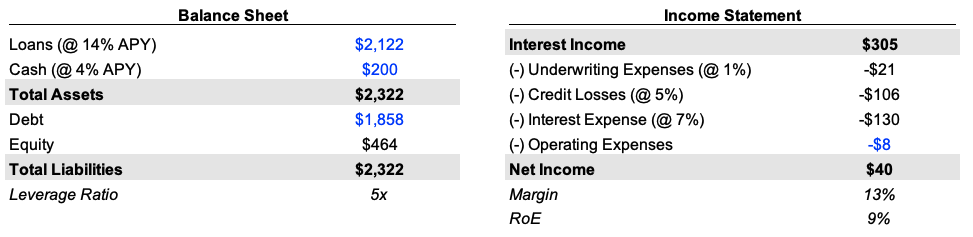

After brushing yourself off, you’re eager to take things to the next level. This is now your third year in business, and you’ve learned the lessons from the first two: now, you only lend to borrowers who live close to you, and who at least two of your friends will vouch for. As a result, underwriting expenses (1%) and credit losses (5%) go back down to year-1 levels. You start issuing fewer, bigger loans ($50), which allows you to fire your assistant and save on salaries. You still haven’t given yourself a raise, but with these changes in place, you tell your investors you expect to generate a 25%+ return on equity this year.

By the time you’re out deploying the capital, the playing field has shifted once again. After seeing you ask for bigger loans three years in a row, the bank figured out what you are up to and mailed loan offers to every house in the neighborhood at 12%. Bastards. Your friends still borrow from you - they like you, and the fact that you drive to them - but when you get there, with their bank letter in hand, they’re only willing to pay a 14% rate. At year-end, you sit down to write a letter to your investors. After a year of hard work growing the business and making it more efficient, you generated a flat $40 in profits and a 9% RoE.

Year-2 starting balance sheet and year-3 income statement for our illustrative lending business.

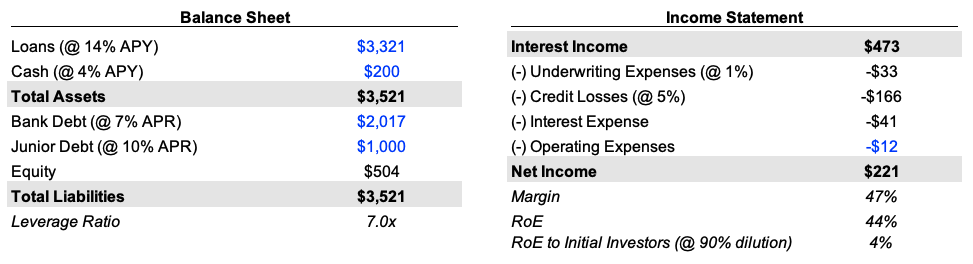

Year four rolls around, your hair is starting to gray, but you’re hell-bent on winning. You join a gym and find a new pool of trusted friends to lend to, and hire back your assistant. You find a local family office to loan you another $1,000 on top of the bank, increasing leverage from 5x to 7x. In June, you’re feeling damn good: the loan book is healthy and growing, and both losses & expenses are under control. You write in your mid-year letter to investors: “After four tough years, we have finally found our groove: I think we will grow profits more than 5x this year to $221 and generate an outstanding 44% RoE.”

A few months later, disaster strikes. The local factory goes on strike. Many of your gym friends, lacking a paycheck for the foreseeable future, ask for an extension. At first, you’re not worried—you tell investors: “Our borrowers are good for the money, they just need a few months max for the strike to end. In the meantime, our $200 cash buffer is enough to pay the interest expense on bank debt for over a year.” You believe it too, until an email lands in your inbox from the family office’s general counsel. Tucked into the footnotes on page 29 of the financing docs, they have the right to accelerate repayment of the loan from twelve months to three months under certain technical conditions—one of which you recently breached.

A week goes by that feels like a year. You sit on the email from the family office, buying time to come up with a gameplan to raise capital elsewhere and repay the loan. With the strike showing no signs of slowing, you get another email. The subject: Loan Extension. In the email, the family office offers to extend the loan for a year, under one condition… you sell them 90% of your company at a fire sale price. You ask your neighbors for a bridge round to gain some negotiating leverage, but after three and a half years of disappointing returns, they all pass. With no other options, you take the family office deal. At the end of the year, the promise you made to investors only came half true: the business did indeed generate $221 in profits and a 44% ROE, but after dilution, you and your neighbors’ return on equity was only 4%. Meanwhile, the family office increased annual returns from 10% on their initial loan to over 16% including dividends from their shares. Their lawyer gets a bonus while you’re still stuck making $8 a year.

Year-3 starting balance sheet and year-4 income statement for our illustrative lending business.

If you’ve built or invested in a lending business before, the story above probably looks familiar… just add a few zeros to the dollar figures (and if it’s not familiar yet, you’re about to have an interesting few years!). It is an admittedly oversimplified, but representative tale of hundreds of lending businesses that failed to generate attractive returns for early investors due to the structural challenges of the lending business:

- Adverse selection: growth requires constantly expanding to new cohorts of borrowers, which you likely don’t understand as deeply or can’t serve as cheaply as your initial customer base.

- Competition: as you scale, other lenders (in fact, often your own lenders) become aware of your outsized profits and push to aggressively enter the market, compressing yields for everyone.

- Tail risks: as leverage increases, lenders demand more restrictive controls and covenants over your cash flows. Eventually, an exogenous shock that dries up liquidity can make you insolvent.

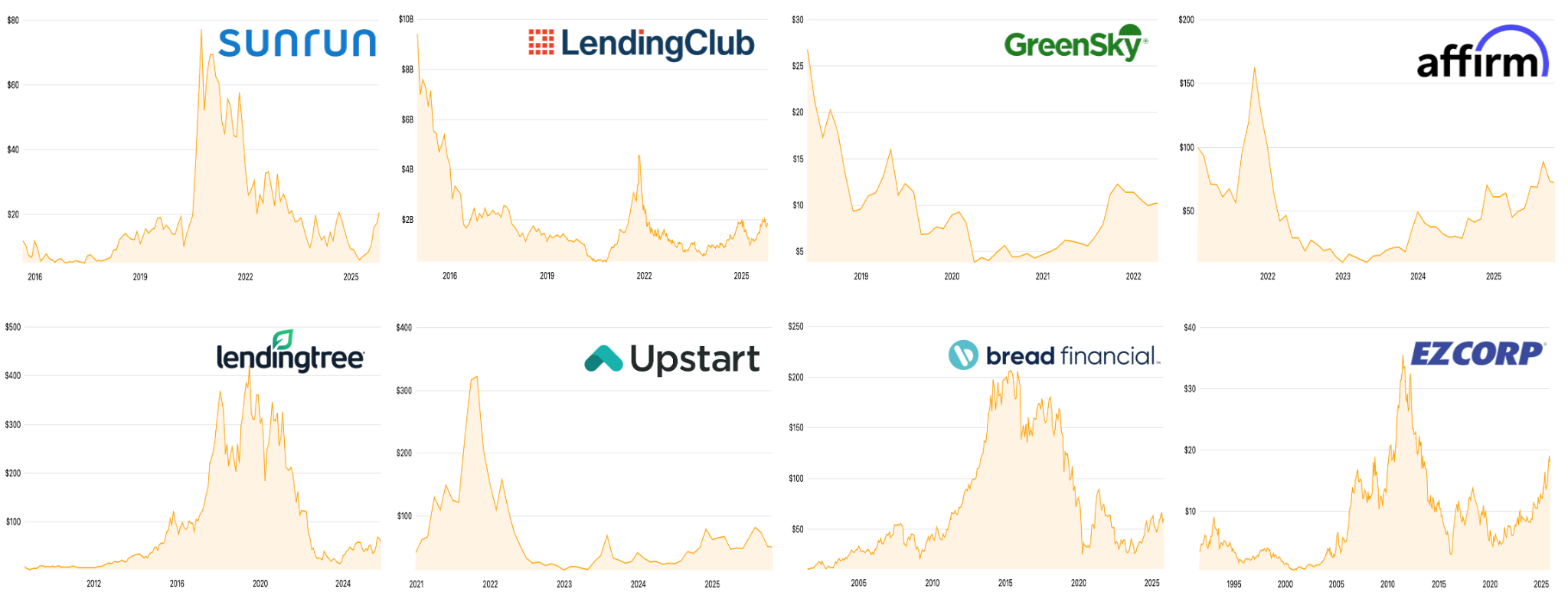

Below are just a few examples of lenders that destroyed billions of dollars of equity value over the past decade and left a sour taste in the mouths of public markets investors, who are now generally skeptical of tech-enabled lenders and value them at lower multiples than software or marketplace businesses.

Select lending businesses’ share prices. Source: companiesmarketcap.com.

IPOs themselves are a large part of the reason for poor public markets performance of lenders. Going public requires sharing granular internal data with investment banks who have massive credit origination and capital sourcing teams working in the same building as your “advisors”. While there is a Chinese Wall in theory, in practice bankers switch jobs and data about the key drivers of your business leaks. It takes a few years for the bank to spin up competing products, but eventually their distribution and balance sheet dominates and your business tanks. If for some reason the bank doesn’t want to compete in your industry (e.g., gambling or cannabis) and you start making lots of money, eventually a desperate executive at some payments, lending, or fintech seeking growth will spot your public financials and look to compete.

In the private markets, entrepreneurs have built some monster lending businesses. The three biggest lenders started post-2017, Figure for real estate (HELOCs), Upgrade for consumer (unsecured), and Goodleap for residential solar, have collectively originated $85B of loans and created nearly $30B of shareholder value over the past eight years. The first recently went public, the second announced plans to IPO in the next 12-18 months, and the last remains private. All of them are massively profitable, generating nine figures of earnings (for some, free cash flow). They overcame the challenges faced by our illustrative lending business and came out stronger. How? Leveraging speed and securitization.

The most profitable lending businesses are structurally faster than competitors. For direct originators, borrowers are willing to pay higher rates to lenders that put cash in their pockets faster and with less hassle. For partner-led originators, a distribution partner will show the fastest quote to users in order to increase conversion and secure a commission, rather than wait for slower quotes at a potentially lower price. Figure, Upgrade, and Goodleap all started around 2017 and were among the first to build digitallynative backends capable of originating, underwriting, and funding a loan in days rather than weeks.

The second key moat is securitization. You know the saying “first-time founders focus on product, repeat founders focus on distribution”? For lenders, it’s more like “first-time founders focus on the top half of the balance sheet (assets), repeat founders focus on the bottom half (liabilities).” The lenders that survive long enough to become big businesses carefully architect their funding sources to reduce the reliance on any single lender for capital needs and minimize credit and duration risk. The typical path looks like this:

| Originations | Equity | Credit | Cost of credit |

|---|---|---|---|

| $50K-$100K per month | $500K-$1M preseed | None, lending from equity | 40-50% |

| $100K-$1M per month | $3M-$5M seed | $1M-$10M bank loan or warehouse facility | 20-30% |

| $1M-$10M per month | $12M-$20M series A | $10M-$50M forward flow agreements | 15-20% |

| $10M-$50M per month | $50M-$100M series B | $50M-$100M forward flow agreements | 12-15% |

| $50M-$150M per month | $100M-$200M series C | $100M-$250M unrated securitizations | 8-12% |

| $150M+ per month | $250M+ series D or IPO | $250M+ rated securitizations | 5-8% |

Note: cost of credit assumes today’s EFFR of ~4%.

At first, you fund loans with an expensive warehouse or revolving credit facility, or a term loan, all of which require giving up a senior lien on your entire company. These might cost 20-30%, or a bit lower if you’re willing to personally guarantee the debt. As you begin to scale and have a few months of positive loan tape data, you go back and negotiate successively bigger facilities at lower rates (sub-20%). After a year, you begin building relationships with hedge funds and asset managers and negotiate forward flow agreements whereby they agree to buy $10M+ of loans over a year at mid-teens yields, assuming loans continue to meet certain criteria (e.g., 600+ FICO). If the loans don’t meet those hurdles or losses come in higher than expected, you (the originator) keep them on your balance sheet and eat the losses. As more and more data rolls in, you go back to the asset managers and convince them to increase commitments to from eight figures to nine figures. At this point, you have funding necessary to originate mid-eight figures of loans on a monthly basis ($10M+) and you start building relationships with banks and insurers.

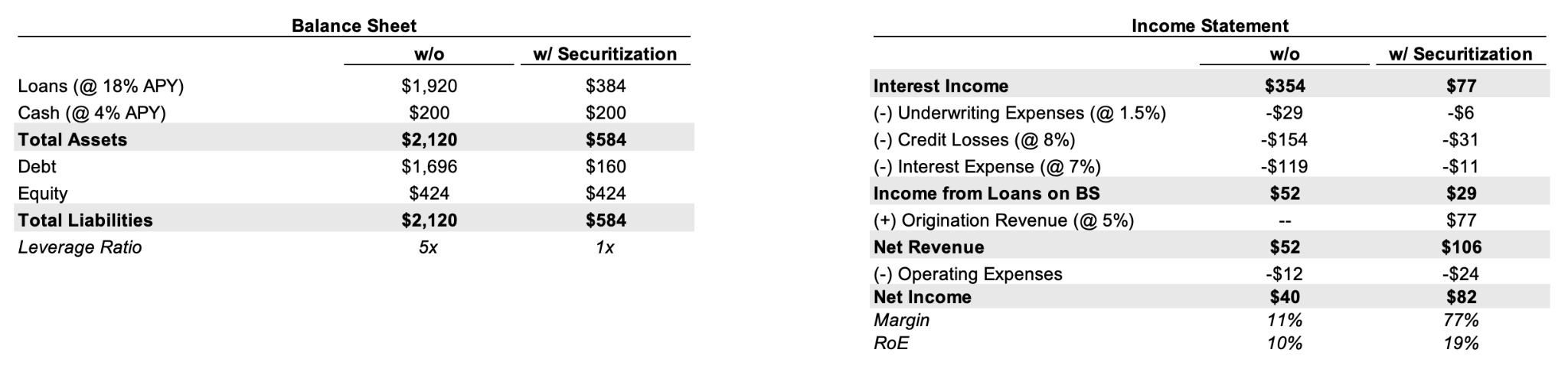

Rated securitizations are the final boss of TradFi credit. In a securitization, a lender (originator) packages a block of loans into an SPV, and sells interests in the SPV to banks, insurers, and asset managers for cash upfront. Credit losses are socialized among SPV holders rather than the originator’s shareholders. For a sense of economics, below is what our lending business above would have looked like in year two (when losses spiked) if 80% of loans were securitized and only 20% were held on balance sheet. Assuming a 5% fee on originations which drives revenue (and cash!) immediately, margins increase sevenfold and return on equity doubles due to the capital-light business model that securitization enables.

Year-1 starting balance sheet and Year-2 income statement for our illustrative lending business.

In addition to the theoretical benefits of a better fundamental business model, securitization provides the pragmatic benefit of accessing much deeper and cheaper pools of capital than private credit. SPVs can be sliced up into several risk-based tranches with different breakpoints in the credit waterfall. Certain tranches can be held on banks’ and insurers’ balance sheets with less regulatory capital reserves held against them than private credit and other alternative assets. This provides a structural advantage in funding costs for lending businesses, since regulated banks and insurers will pay higher prices for notes if holding them frees up balance sheet capital to invest in other, higher-yielding assets. The caveat here is that securitization requires scale: across bankers, lawyers, accountants, trustees, and ratings agencies, launching a securitization will run you $2-3M in fees at a minimum, which means issuances smaller than $200M are not viable. Unrated securities can be done somewhat cheaper, say for $500K-$1M in fees, but you lose the structural regulatory advantage described above.

Over the past year, Goodleap, Figure, Upgrade have all issued rated securities of $300M-$400M, with banks and insurers bidding up the investment grade tranches down to 5-7% yields. Securitization is the moat that has allowed these companies to stay ahead of subscale fintech lenders who are stuck selling loans in forward flow agreements at 12-18% yields. So, how can any new lending startup compete?

Onchain is faster than Digital. Tokenization is faster than Securitization.

Crypto-enabled lenders will beat the prior generation of tech-enabled lenders at their own game: speed. In a few years, borrowers will be able to choose between fintech lenders that put money in their hands in at best a few days, and crypto-enabled lenders that collect user data via zkTLS, underwrite borrowers via AI, and make payments via stablecoins, and are therefore able to put money in users’ hands in minutes. Putting money into users hands faster than competitors mitigates adverse selection, since all borrowers and not disproportionately the ones with a poor credit profile - prefer getting money in their pocket faster. It might seem counterintuitive, but a faster lending business typically has both higher rates (users pay a premium for speed) and lower losses (less adverse selection) than a slower one, all else equal.

What’s even more counterintuitive is that faster lending businesses are also safer than slower ones. Understanding why requires a bit more context on how traditional asset-backed securitizations work. Typically, a lender like Goodleap or Figure will originate thousands of loans over the course of a month, drawing on a senior (corporate-level) revolving credit facility from an investment bank to fund them. Once originations reach a critical mass, say $250M, the syndication desk at the bank takes over and analyzes loan tape data, creates a prospectus, and engages ratings agencies in a process that takes at least 3-4 weeks. Once the issuance is rated, the bankers do a roadshow to pitch the securitization to banks and insurers, collect indicative bids, and set coupons and allocations at market-clearing levels for each tranche. This process takes at least another 3-4 weeks, after which the proceeds are used to pay down the lender’s revolver at the bank. The “cycle time” for the TradFi securitizations market is 6-8 weeks.

A lot can happen in 6-8 weeks! On January 28, 2020, UK-based fintech lender Funding Circle closed a $250M securitization with A-/A3 ratings from Kroll and Moody’s. Three days later, the US declared a public health emergency due to coronavirus, and three months later, Funding Circle shut down its loan marketplace and told its investors, “the businesses you have lent to are good, creditworthy businesses and we expect returns to remain resilient over the coming period.” Sound familiar? By August, the notes had been downgraded with agencies citing credit losses running at almost double the expected pace.

More recently, in June, Kroll awarded AAA rating to the senior tranches of a $217M securitization from Dallas-based subprime auto lender, Tricolor. In June, Kroll proudly wrote (emphasis ours):

“KBRA applied its Auto Loan ABS Global Rating Methodology, as well as its Global Structured Finance Counterparty Methodology and ESG Global Rating Methodology as part of its analysis of the static pool data and the underlying collateral pool and stressed the capital structure based upon its stress case cash flow assumptions. KBRA considered its operational review of Tricolor, as well as several business updates with the Company since that time. Operative agreements and legal opinions will be reviewed prior to closing.”

Despite three methodologies, three analyses, and three reviews, Kroll somehow managed to miss that Tricolor was re-pledging loans as collateral at multiple different banks. On September 10, as investment bankers in NYC were actively soliciting demand for Tricolor’s securitizations, the company filed for Chapter 7 bankruptcy. The bankers were in a tough spot, having lent the company $500M+ in warehouse credit lines secured by potentially fraudulent loans. The next day, on September 11, the notes that Kroll had called “investment grade” just three months ago were trading at 78 cents on the dollar; junior tranches traded as low as 12 cents. Unable to clear the notes of their books, Tricolor’s banks - JPM, Fifth Third, Barclays - took half a yard in losses and had to explain the embarrassing situation to shareholders.

The tales of Funding Circle and Tricolor make it obvious why tokenization is safer than securitization for both sellers and buyers of loans. The key advantage is again speed. While assets securitized by Wall Street have a clock speed of 6-8 weeks at best, blockchains have a clock speed of 12 seconds at worst. For sellers of loans (originators), this means clearing loans off the books between four-hundred thousand times (for Ethereum) and twelve million times (for Solana) faster than fintech lenders. This massively reduces inventory risk since credit risk is transferred to its ultimate owner in near-real-time onchain. Tokenization is not just safer, but also much cheaper: it replaces an army of expensive bankers, lawyers, accountants, and trustees with smart contracts that can serve near-infinitely many issuers at near-zero marginal costs. For buyers of loans, tokenization provides stronger guarantees of claims over collateral enabled by transparency. In TradFi, where it takes months from the time a loan is originated to when it is bought, the chain of custody becomes hazy: unscrupulous originators like Tricolor might double or triple pledge the collateral. It’s a lot harder to do that when loan buyers have visibility into the underlying collateral and/or cash flow data in seconds rather than months after origination.

We believe speed is the ultimate virtue for lending businesses—it absolves almost all other sins. Lenders that underwrite and disburse loans quickly attract a bigger pool of high-quality borrowers and charge them higher rates. Lenders that clear loans off their balance sheets faster are more likely to survive credit shocks and provide loan buyers with stronger, code-enforced claims over future yield.

In the context of credit markets, tokenization is simply a faster and better version of securitization. This isn’t a prediction we think will happen, but a phenomenon we see happening in real time. Onchain credit markets are already more scalable than offchain securitizations: Ethena (+$3.6B, even after the 10/10 crash) and Maple (+$2.9B) each individually added more liabilities this year than the entire US residential solar asset-backed securities market (+$1.5B as of July). More than $100B of new stablecoins have been minted YTD in 2025, with two months still left to go. As real rates continue to fall, the flow of stablecoins being minted and deposited into onchain credit / yield-bearing vaults will accelerate further.

2017 presented a unique window of opportunity to build new TradFi lending businesses. Cloud computing was mature enough to power a 10x better customer experience at scale (loans in days rather than weeks!), but had not yet been adopted by incumbents. On the liabilities side, after almost a decade since the financial crisis, Wall Street had once again regained its appetite for securitized products. The confluence of technologies including AI, stablecoins, and zkTLS provides that same opportunity in 2025.

In the following installments of this series, we discuss what we believe to be the biggest opportunities available in onchain lending today. Check out part 1 and subscribe here to get the rest.