Liquid Markets

Investor confidence in liquid crypto markets is officially back. After a volatile 2023 marked by three separate >15% corrections, crypto ended the year as the top-performing global asset class with market cap recovering from $850B to $1.8T. With upcoming US presidential elections, accelerating government deficits, and the emergence of CBDCs, we expect continued relative macro strength for crypto going into 2024, with flows disproportionally benefiting category leaders in emerging sectors (DePIN) and established leaders that have re-invented themselves throughout the bear market (Alt L1s).

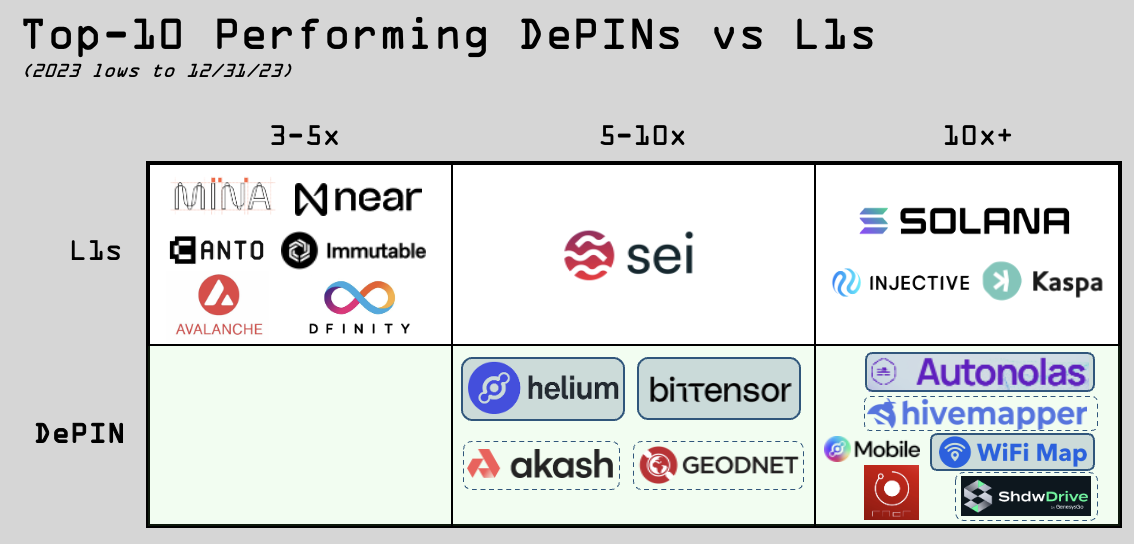

Measured from 2023 lows, the former has proven to be the more fertile hunting ground: DePINs saw six of its ten top-performing liquid assets returning 10x+ and another four returning 5-10x throughout the year. Smart contract L1s saw only three of its top-ten performing assets returning 10x+ and one asset returning 5-10x. Given the massive relative valuation gap between the two sectors - $20B DePIN market cap vs $500B for smart contract L1s - we expect DePIN to continue to produce an outsized number of outsized winners in the liquid crypto markets. We’ve built core positions (defined as >$1m NAV at Q4’23) in four of the top-ten performing DePIN assets and non-core positions in another four.

Solid box represents EV3 core position; dotted box represents non-core position. While our long-DePIN positioning drove the bulk of performance vs broader crypto benchmarks, our insights from governance & onchain data drove the bulk of performance within DePIN. We’ve been ideologically long Helium since the launch of EV3 almost two years ago (with $HNT trading above $20) but didn’t start building a position until at a cost basis. By then, the key questions around Helium’s renaissance had been de-risked: Helium Mobile had already shown evidence of consumer virality in Miami (>5k subscribers paying $5/mo), the network was already offloading data via carrier-grade WiFi (which carries far less technical risk than CBRS), and the timing for the nationwide rollout was being openly discussed on monthly community calls. Today, Helium Mobile boasts >30k subscribers and $HNT trades around $6 ($0.9b market cap). As the crypto-MVNO flywheel gains steam in markets across the US, we think Helium has a lot more room to run.

Learn more about our Helium thesis from our 2022 letters here, here, here, and here.

Bittensor, a crypto-network that incentivizes machine intelligence, landed on our radar after its native token rose 3x in Q1’23. While the network was nascent in many ways (user applications, wallet infrastructure, exchange liquidity), by our estimates miners had spent ~$10m in aggregate model training costs to mine $TAO—roughly comparable to the $12m that OpenAI spent training GPT-3 in 2020, but an order of magnitude lower than the $100m+ spent training GPT-4. By Q3’23, discussions with leading miners in the ecosystem caused us to refresh our estimates to >$30m in cumulative training spend. More importantly, we saw miners aggressively hiring AI developers ahead of an upcoming network upgrade that would enable the creation of permissionless (and potentially highly lucrative) subnets on top of Bittensor. We doubled down on $TAO in at a cost basis, concurrent with the Revolution upgrade and the first third-party products going live. Today, there are 32 subnets building unique AI products on Bittensor and $TAO trades around $250 ($1.4b market cap). As the number and caliber of AI developers in the ecosystem continues to skyrocket, we believe Bittensor has the potential to be one of the most important permissionless networks on earth.

Learn more about Bittensor in our interview with co-founder Jake Steeves.

Braintrust is a crypto-powered marketplace for freelance talent with >$200m in cumulative gross sales. Braintrust grew extremely quickly & reasonably efficiently to $28m in gross sales on only $24m capital raised, then in Dec’21 raised a monster $100m token round led by Coatue & Tiger Global. Since then, the number of active freelancers on the network is up from 3.6k to 370k, cumulative gross sales are up from $28m to $205m, and the surge in AI-related hiring is driving tailwinds (e.g., Scale AI filled 40 roles through Braintrust in Dec’23). Despite all this, $BTRST fell from $3 to below $0.30 as growth investors exited their crypto positions, and today Braintrust trades at a mere 45x multiple of annualized onchain revenues—within spitting distance of its web2 competitor Upwork which trades at 37x annualized operating cash flows. We have personally hired & fired at least two dozen freelancers over the past two years and found one consistent trend: Upwork freelancers nearly always request to be paid off-platform to avoid fees & payout delays—a request we’ve never heard from a Braintrust hire. Given Upwork/Fiverr are each 5-10x bigger than Braintrust today, Braintrust can compound for years simply by eating away market share from web2 competitors. The real prize, however, is becoming the category leader in a market which is effectively TAM-unconstrained: global knowledge work.

Over the past few weeks, Braintrust migrated 34k user wallets from Ethereum mainnet onto Coinbase’s new L2 to become the first & largest DePIN on Base. In the short-term, we expect this to drive renewed attention to $BTRST as the category leader on Base, especially with DePIN use cases being cited as a key driver of renewed attention on Solana. On a longer time frame, Base’s lower fees & higher throughput allows Braintrust to put more of the network’s critical activities onchain, creating an opportunity to transform from a two-sided services marketplace ($10b+ opportunity) to an onchain professional social network ($100b+ opportunity). Learn more about Braintrust in our interview with co-founder Adam Jackson.

We made several smaller liquid bets in Q4, many of which are highlighted in our State of DePIN report. Going forward, we will disclose individual liquid investments in our quarterly portfolio summaries only after fully sizing our position.

Private Markets

If there’s a single encapsulating word for the difference between traditional and crypto market structures, it’s reflexivity—a direct result of protocol composability and shared global settlement. The impact of reflexivity is felt almost immediately in the liquid markets, but the effect on private crypto markets is even more profound. As token prices recover, protocol treasuries fund more grants for entrepreneurs in their ecosystems; miners reinvest more of their earnings into scaling the network’s supply-side faster; and both web2 & web3 partners move quicker to integrate products & spur new demand. We are seeing clear signs of crypto’s reflexivity benefiting the early winners in our private portfolio, which continues to be our primary focus in generating asymmetric fund returns.

As one example of the reflexivity, consider that two of our portfolio companies - Petastic & MintStars- raised at least half a year’s worth of cash runway and subsequently leveraged the extra runway to meaningfully extend the efficiency of our seed dollars. Petastic partnered with animal shelters across the country to register 600k+ pets onto their blockchain-based pet identity platform. MintStars onboarded 3k+ fans onto a creator platform that quietly runs on NFT/stablecoin rails. Both companies are growing organically at 20%+ MoM with the momentum to fundraise from a position of strength in ‘24.

Our portfolio compan y WiFi Map launched the $WIFI token in Apr’23. Since then, ~250k users have earned $WIFI for adding public WiFi hotspots and running speed tests, the validation quality of the network (measured by speed tests per week) has more than doubled, and $WIFI tokenholders have benefited from >$850k of onchain revenues generated from in-app eSIMs sales & subscriptions. $WIFI is up +60% since the initial listing, and with 5+ million MAUs we continue to believe it is one of the most undervalued networks in crypto.

We made three new private investments in Q4 into Sovrn, Zonal & Lumino Labs:

Sovrn is crypto infrastructure company co-founded by three of the earliest engineers & designers hired at Dimo, where they helped build the core product that has since scaled to >30k connected onchain

vehicles. Sovrn is building a portable identity primitive that enables developers to permissionlessly & securely tap into user data from any existing web2 platform. Computation happens locally on users’ devices using advanced ZK & MPC cryptography, ensuring that private data has no possibility of being leaked or faked. The effect on DePIN is profound: Sovrn enables vampire attacks on web2 businesses, allowing entrepreneurs to bootstrap crypto-networks with reputation, in addition to capital and labor. For example, Nosh (decentralized food delivery) can implement a 10x rewards multiplier for drivers with 5-star Doordash ratings, using Sovrn as a filter to concentrate token incentives among the highest-quality drivers in a given market. In a world dominated by power laws, luring away the top-decile of users from a marketplace is akin to knockout punch to the gut: though they might throw a few punches on the way down, defeat is all-but-guaranteed. We believe this will drive an entirely new era of the consumer web, where ‘walled gardens’ become irrelevant as power users are armed with portable ‘digital ladders’ in their back pockets. To be explicit: our long-term view is that any web2 marketplace whose primary moat is a reputation graph is a melting ice cube with no terminal value. We invested in Sovrn at a post-money valuation cap.

Zonal is a decentralized mesh positioning network founded by former engineers from Microsoft & the Chia Network. Leveraging the latest generation of wireless chips inside modern smartphones (UWB/ultra- wideband and BLE/Bluetooth low-energy), Zonal aims to enable Apple ‘find-my-iPhone’ style functionality on top of an open, decentralized network. Zonal use s BLE stickers to offer a solution that is orders of magnitude cheaper than LoRa- or GPS-based systems. These stickers harvest power from ambient radio waves, meaning they offer ‘unlimited battery life’ and cost as little as $0.10 given the lack of physical battery. For comparison, the leading sticker-tracking solution on Helium LoRa costs $14 per sticker and has a useful life of 1 year, with no ability to recharge or replace batteries. The tradeoff comes in the form of effective range: 10m for BLE vs 1km for LoRa (or anywhere-with-a-clear-sky-view for GPS). Zonal’s initial focus is on exploring positioning use cases that support such density. For example, as an initial use case Zonal is partnering with our portfolio company Petastic to offer the lowest-cost pet tracking solution on the market. Whenever one of the >600k pets on Petastic gets adopted, pet parents will receive a free Zonal sticker attached to their pet’s collar. If the pet gets lost, the owners can activate a ‘beacon’ within the Petastic app and get notified whenever another device on Zonal’s network passes within 10m. We invested in Zonal at a post-money valuation cap.

Lumino is a decentralized GPU marketplace built by two top technical minds out of the Filecoin ecosystem. Lumino brings many GPUs on day one, with a strong negotiated demand pipeline that will see them scale to low-seven figures quickly. While GPU compute marketplaces is likely the most crowded vertical in DePIN, we believe scale and demand pipeline are key early differentiators that will separate the consolidators from the consolidated in ’24-‘25. The vast majority of the >50 compute platforms we’re tracking today have no real supply-side capacity, and the ones that do are valued an order of magnitude higher than Lumino. In addition to their relationships within the Filecoin ecosystem, Lumino is working with other DePINs (including our portfolio investments Ritual and Autonolas) to bring low-cost compute into their ecosystems. We invested in Lumino at a post-money valuation cap.

2023 Lessons

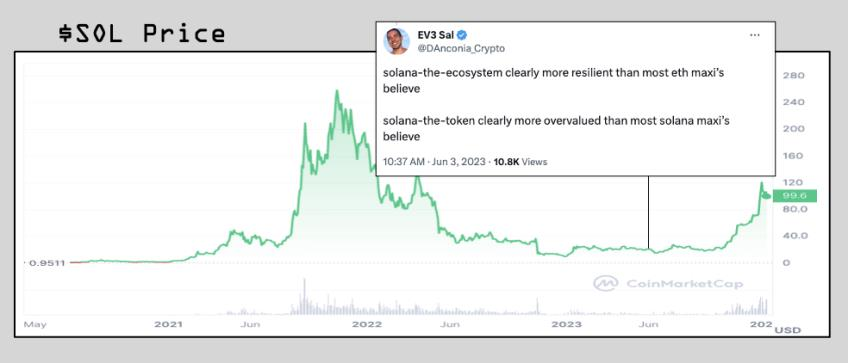

As venture investors, our biggest mistakes will be borne of omission, not commission. The decisions we lost the most sleep over in 2023 are those where opportunities should have been obvious to us, but where we failed to act with conviction anyways—namely Autonolas, Solana, Hivemapper & Render.

Most of you will have read Seth Klarman’s old anecdote about sardine trading. In case you haven’t, it goes something like this: a businessman, visiting a port city in California, stops by a restaurant for lunch and orders the sardines. Sardines had recently disappeared from the local coasts and prices for incoming shipments had gotten bid up to absurd levels by commodities traders. The businessman finished his lunch, and - upon receiving a bill for $1000 - immediately becomes ill. The waiter, unsure whether the businessman is sick from the sardines or the bill, responds: “You don’t understand—these are not eating sardines, they are trading sardines.”

In 2023, we made the inverse mistake to the businessman in Klarman’s parable. We visited the port of Solana at the NYC hacker houses in April (with $SOL below $20) and again at Breakpoint in Amsterdam in October (with SOL below $30). Everywhere around us, we saw developers eating the sardines—from local street vendors (hackathon teams) to large-scale franchises (Helium/Render migrations), and from grocery stores (DePIN) to snack stands (payments) to bars (gaming). We even spotted a few locals trading amongst each other with prices denominated in sardines. Despite seeing all this, we looked over at the horizon, saw cargo tankers full of sardines floating in the bay (upcoming forced $SOL sellers from the FTX estate) and decided it wasn’t yet the right time to take on a position. Since then, $SOL is up 5x despite the FTX estate having market-sold significant amounts of $SOL, and Solana has made significant headways to position itself as the leading L1 for DePIN.

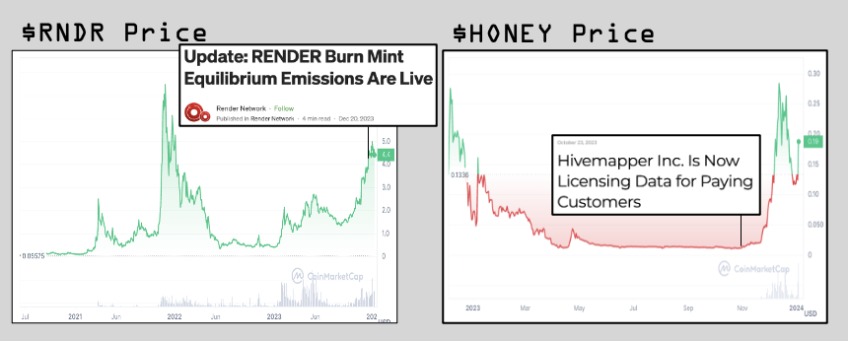

Missing Solana was our most painful mistake because we already knew how to avoid it. Render & Hivemapper were bigger misses from a financial perspective, but less frustrating since we’re able to adjust our investment process in response. We had always liked Render & Hivemapper as businesses - and even hosted the founders of both projects on our podcast - but we had never gotten comfortable owning tokens in networks where the economic terms between the founding corporation & the DAO are not clearly defined. Unlike the Helium/Bittensor/Braintrust situations, where we had time to react to early onchain data, $RENDER re-priced from $100m to $1.7b market cap before posting a single dollar of onchain revenues. $HONEY started posting onchain revenue in September but was initially burning tokens from genesis allocations rather than tokens purchased off the open market— this is highly disadvantageous to tokenholders, since companies can sell out of their genesis allocations while preserving the equity value of the centralized company (for further discussion, see State of DePIN page 10). Hivemapper claimed to migrate to a more tokenholder-friendly buyback policy on Nov 1, but we

were not able to validate the claim with onchain data before $HONEY rose 10x in twenty days starting Nov 20. In both cases, we learned that the marginal token buyer today is willing to overlook weak tokenholder rights to own a piece of a network with a category-leading product.

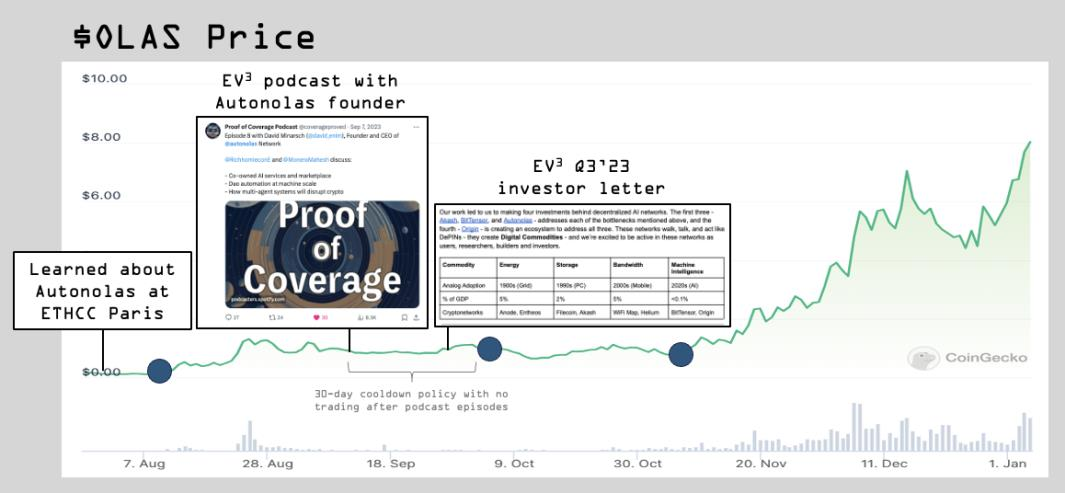

Our final heartburn-inducing mistake of the year - Autonolas - was an error of sizing. When we wrote to you about Autonolas in our Q3’23 letter, $OLAS was trading around $1 and had risen 10x over the preceding two months. We built a small position with an eye towards doubling down opportunistically at better prices. Unfortunately, we never got the chance to buy-in meaningfully below our initial entry and deployed only ~$100k at cost. Two months later, $OLAS is trading above $8 and our non-core position, now worth north of $1m, is driving meaningful unrealized gains for the fund—but could have been much more impactful to returns if we were quicker to put on a full-sized position upon building conviction.

Blue dots represent EV3 transactions.

XNET, our biggest position by cost, is a DeWi network focused on neutral-host offload. Unlike Helium, XNET does not serve customers directly: instead, they aim to incentivize wireless deployments that can serve a multitude of different use cases on a single interoperable network. Neutral host CBRS requires deep technical integrations and has yet to be implemented at scale, and the adoption ramp has been slower than we’d hoped: XNET’s negotiations with a national telco were interrupted by a merger, and Helium pivoted away from CBRS to focus on lighter-touch WiFi offload. We continue to believe CBRS is the “end game” for US DeWi due to its superior propagation characteristics vs WiFi and its established priority licensing regime. Unfortunately, Dish’s quest to build a fourth US telco is looking

dimmer than ever, and with it goes any hope of telco-driven competitive innovation in the coming years. With telcos unlikely to pilot new tech, XNET is focused on partnering with cable companies to offload traffic from mobile subscribers on their fast-growing MVNOs (e.g., Spectrum, Xfinity, Cox Mobile). Some of these businesses are larger than Dish and have proven to be far more collaborative than telcos. We remain optimistic about XNET’s future as initial customers roam onto the network in 2024.

2024 Predictions

What’s next for DePIN as we look out to 2024 and beyond? If you’ve made it this far into our letter, we’d like to leave you with five DePIN predictions that are at the front of our mind today:

1. Layer-1 Wars: One or two base layers will cement their position as ideal venues for DePIN projects, driven by low transaction costs, high uptime/reliability, and deep liquidity & composability. We predict more DePINs will be built on general-purpose L1s (Solana) and L2s (Base) in 2024 than on DePIN-specific L1s (IoTeX/Peaq) and app-rollups (Caldera). 2. Wireless: DeWi will make a resurgence in ’24, with Helium Mobile’s flywheel accelerating throughout the year to reach 150k+ subscribers by end of ’24 and 500k+ subscribers by end of ’25. Given the location-based nature of DeWi, Helium won’t be the only winner: Really will fast-follow with their own WiFi-offload powered MVNO in Austin, acquiring 10k+ subscribers by year-end. Lastly, crypto markets will come to understand the fixed wireless business model, bidding one of the new fixed wireless token launches up to $1b+ FDV (Andrena $ANET and Althea $ALTG). 3. Compute-over-Data: Storage and compute, previously separate silos within crypto, will finally converge as verifiable computation over local user data in a trustless manner becomes possible. Filecoin has been an ecosystem leader here and momentum is accelerating, with an endgame of driving the next generation of AI products that comply with data sovereignty requirements and leverage growing edge compute capabilities globally. We predict that compute networks will continue to be the biggest category of DePIN by both revenues & market cap at year-end 2024. 4. Mapping: The gamification of mapping networks like Hivemapper and WiFi Map will bring millions of new users into DePIN. These networks combine low-effort contributions and pass the ‘toothbrush test’ (products you use at least twice a day: your car & WiFi), creating the right conditions for viral growth. We believe mapping will be the single biggest top-of-funnel for onboarding non-crypto native users into DePIN in 2024, with >1m new users earning mapping tokens as their first crypto. 5. Security: As generative AI powers an explosion of content, the sophistication of hackers/cheaters is outpacing the sophistication of traditional security measures. DePIN is uniquely positioned to solve both physical and virtual verification problems. In physical verification, we expect a gamified geo-positioning protocol to break out, enabling new types of onchain commit-reveal games for real-world location (e.g., WiFi Map using speed tests as a location verification tool). In virtual verification, we expect security finance (SecFi) to emerge as a third major vertical of blockchain infrastructure alongside oracles & RPCs with billions of dollars in aggregate market cap.

Closing & Housekeeping

We will be hosting our first annual investor meeting in May 2024 in New York City and will be sending out further details at the end of the month. We plan to continue the schedule below for fund document distributions:

- Marks 30 days after quarter-end

- Quarterly letters & balances the fortnight following quarter-end

- Annual reporting & balances the first week of April

As always, we are eternally grateful for your support and encouragement.

Your partners,

Sal & Mahesh