Dear Partners,

Crypto ended the quarter flat with $2.4T of market cap, amidst volatility that saw three distinct >10% drawdowns and subsequent recoveries. While aggregate value was flat, the explosive growth in crypto-asset issuance continues unabated: nearly as many tokens launched in Q3 as in the entire first half of 2024. The DePIN sector ended with $90B of market cap, re-rating from 9% to 15% of alts—a figure we expect to see rise to 25%+ long-term as sector growth continues to outpace the broader crypto industry.

In the near-term, investor optimism for DePIN private deals appears to be approaching exuberance. Q3 marked the first time we’ve felt a negative imbalance between capital and attention vs new high-quality founders and ideas in DePIN. The lowest rung of excess returns has been squeezed out, with pre-seed valuations rising from $6-8m to $12-15m and a handful of breakout late-stage networks raising at pre-token launch valuations above $500m. Our Fund I portfolio companies took advantage of the favorable financing environment to bolster cash reserves, including five companies that raised follow-on funding at valuations 2-3x higher than our cost basis and extended their runway to 24-36 months.

We deployed into private markets, making it our second-most active quarter ever, with the bulk of capital going to follow-ons into our top-performing existing portfolio companies.

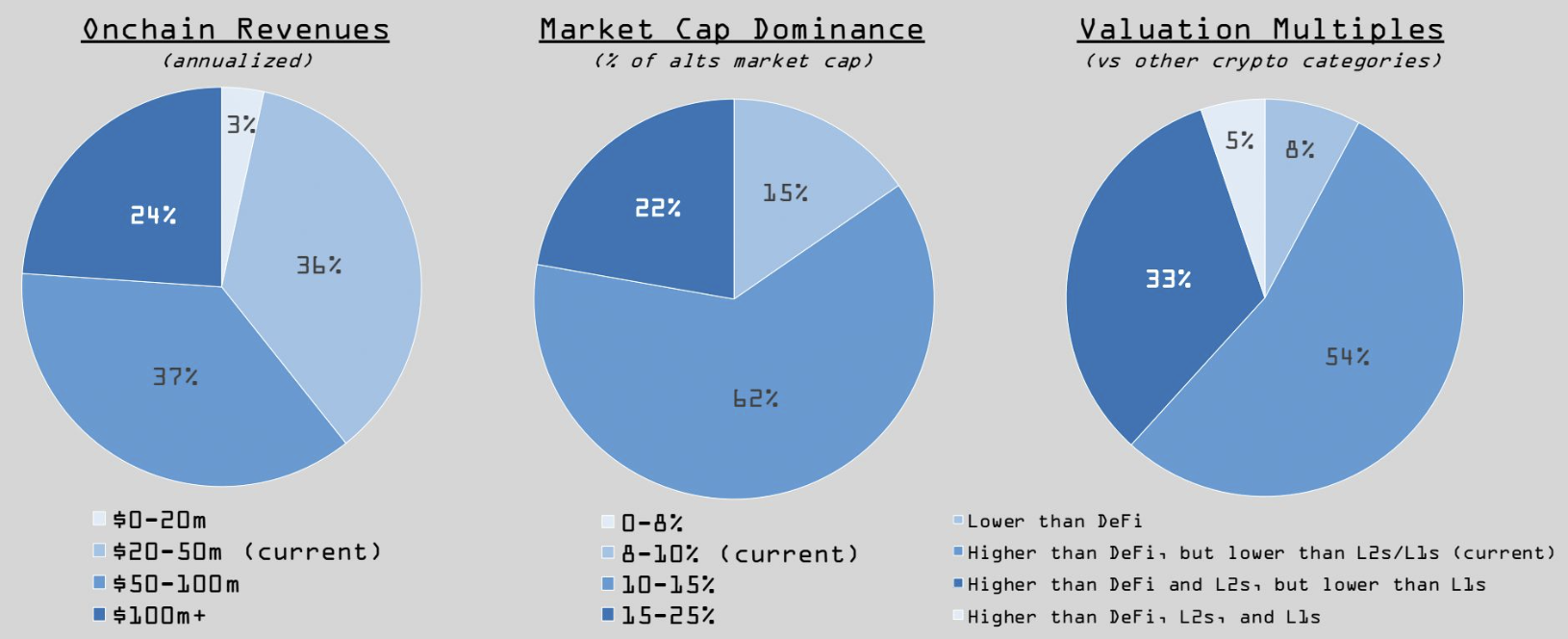

Bittensor and Helium - meaningfully outperformed in Q3, each returning +120% as markets began to recognize the emerging signs of network effects in category-leading DePINs that we wrote to you about in our prior letter. Helium added +20k new subscribers to its low-cost cell phone plan in Q3, while launching its long-awaited telco partnerships that already see several terabytes of daily data offload to hundreds of thousands of end-users. Both the first-party (subscriber) and third-party (offload) businesses burn HNT, driving Helium’s onchain revenue multiple down from >1000x to 350x over the past year. On Bittensor, several subnets launched products that are on track to match and eventually surpass the capabilities and performance of closed-source AI, driven by >$4m of daily incentives paid out to AI developers and infrastructure providers. As reflexivity kicks in, higher token prices translate into greater incentives for users, miners and developers to contribute to growing these networks even faster, creating the fuel for the next leg of upside reflexivity. Bittensor is the #29 highest-valued crypto-network and Helium is #69 as of quarter-end per Coingecko. We believe both assets belong in the top 10 as markets realize the potential of unleashing compounding, token-driven network effects on industries where success is measured in the trillions of dollars.

To learn more about our recent investments, check out our memos on Bittensor,Nosh, Daisy and Glow (pw: satoshi).

EV3 Labs & DePIN Summit

We held our second-annual DePIN Summit in August and were grateful to see many of you there. The event saw over 400 leading DePIN founders, investors and researchers attend. The energy in the room was electric: in an industry where conferences are a dime a dozen, DePIN Summit stands out for its intense focus on uniting serious builders and investors - those with real skin in the game - behind a unified vision of accelerating the global infrastructure revolution known as DePIN.

DePIN Summit survey results: 12-month forward expectations for DePIN

For the past two years, the focus of EV3 Labs - our media, technology and events business - has been to cement DePIN as one of the most important sectors in crypto. Today, that challenge is behind us: DePIN is no longer non-consensus in crypto-native circles. Going forward, our job is to legitimize DePIN across the broader capital markets and general public. Ironically, this means moving away from the term “DePIN” - an ode to DeFi - and positioning our portfolio at the broader intersection of real-world industries and tokenized economies. Starting in Q4, you’ll begin to see EV3 content appear in publications like the Harvard Business Review and the Wall Street Journal, in addition to our presence in crypto news.

The DePIN-adjacent thesis we’ve been most excited about is an important new technology called zkTLS that dismantles the digital “walled gardens” that have protected trillions of dollars of web2 market cap for the past two decades. Our portfolio company Opacity is building the zkTLS infrastructure powering five of our other portfolio companies (soon 6!) to bootstrap crypto-networks with verifiable data from web2 incumbents in social media, the gig economy, fintech and more. Fund I has invested across the zkTLS stack - including both infrastructure and related apps - representing a third of private investments.

“The end is never the end. A new challenge awaits.” — Lonnie Rashid Lynn

Private Markets

We doubled-down on four existing portfolio companies in Q3, deploying at a blended entry valuation of and increasing our blended average ownership from to .

DAWN is a decentralized wireless network focused on providing cheap, fast, reliable internet to homes and small businesses via fixed wireless access technology. By deploying autonomous robotic antennas on the rooftops of multi-family and office buildings, DAWN creates a mesh network of “mini-towers” capable of beaming internet anywhere in the surrounding area.

At scale, DAWN allows anyone to purchase on-demand internet access at wholesale prices. For ISPs, this turns their biggest fixed costs (backhaul connectivity) into a variable one. For property managers, it unlocks new earnings streams by becoming mini-ISPs. For consumers, DAWN is like solar panels for internet access: they make an investment into their home that enables ~free access to a core commodity (electricity or internet) and allows them to cut the cord to avoid expensive monthly bills from their utility company or ISP. On a comparative basis, DAWN is an order of magnitude lower cost, easier to install, and quicker to payback than solar.

In Q4’22 we invested in Andrena, a fast-growing startup ISP with a few thousand subscribers who truly loved the product, led by a relentless founder, Neil Chatterjee. Since then, the web2 business has grown roughly five times larger by coverage, subscribers, and revenues, and the company raised >$30m from top crypto investors to build DAWN.

DAWN came out of stealth in August, launching a testnet validator node that amassed a verified user base of >100k contributors in the first week and >500k in the first month. The vision of shared internet infrastructure is resonating deeply both within crypto and more mainstream audiences. For comparison, Helium Mobile took twelve months from launch to reach the 100k subscribers milestone—we believe DAWN will get there even faster. In the coming months, DAWN will launch their network with 5+ launch partners (professional ISPs and datacenters) to bring DAWN-powered internet service to New York City, Philadelphia, Los Angeles and other markets.

To learn more about DAWN, download the validator node and check out recent coverage at DePIN Summit, Proof of Coverage, Messari, Blockworks, and Frictionless. If you have connections with friendly ISPs, datacenters or property managers that are interested to learn more about monetizing their infrastructure via DAWN, please reach out.

Daisy is an influencer marketing network that turns social media influencing from a single-player to a multiplayer game. Through Daisy’s mobile app, influencers can like, comment or repost other influencers’ sponsored content to earn a share of the associated sponsorship revenues. At scale, this creates an “echo chamber” effect whereby sponsored content is far more likely to go viral within the influencers’ combined social graphs, resulting in 25-50% lower acquisition costs for brands vs traditional (single- threaded) influencer marketing.

Daisy has been the fastest-growing portfolio company in Fund I, achieving seven-figure annualized gross revenues less than six months after its founding. In August, brands paid mo to boost content through Daisy’s network of monthly active influencers. The core “boosting” effect is generalizable to any industry: Daisy’s early customers come from e-commerce, entertainment, crypto and other industries with large marketing budgets. Given the level of pull from current and prospective customers in the pipeline, we believe the company is on track to reach in annualized gross revenues by mid-2025.

What has us most excited about Daisy isn’t just growth, but the emerging signs of defensibility we are seeing across the platform. Influencers are beginning to see Daisy as a primary source of income, providing steady cash-flow that helps keep the lights on in between larger, lumpier sponsorship deals. Fast payouts, powered by stablecoins, is the key differentiator for influencers who are used to getting paid weeks if not months after a sponsored post. In August, we began to notice an interesting emergent behavior where influencers were re-investing their earnings back into Daisy to boost their own organic content, effectively turning Daisy into a closed-loop ecosystem where influencers make money from their profiles and then re-invest that income into growing the value of their profiles even further.

To learn more about Daisy, check out their talk at DePIN Summit or our recent investment memo. If you have any connections with portfolio companies in any industry that are looking to lower their acquisition costs on influencer marketing spend by 25-50%, please reach out.

Opacity (fka Sovrn) enables developers to extract provably-verified data out of web2 data silos, using technology called zkTLS to guarantee end-users’ privacy. For example, our portfolio company Nosh leverages Opacity to verify drivers’ Doordash ratings to incorporate into its own onchain reputation scores. Proofs are generated locally at end-user devices, ensuring that 1) platforms like Doordash can’t stop developers from accessing the data without cutting off access to their own users entirely, and 2) no third-parties are ever able to see or store users’ data, beyond what is attested to in the proofs.

The surface area for what Opacity enables is absolutely massive. Historically, crypto-networks are bootstrapped by either capital (see: DeFi) or labor (see: DePIN). Opacity enables, for the first time, onchain networks to be bootstrapped by a third type of asset—reputation. We have five portfolio companies bootstrapping networks with reputation, with more to come:

- Nosh verifies drivers’ Doordash ratings and offers boosted rewards for top drivers.

- Daisy verifies the attribution of social media engagement across various influencers.

- MintStars offers “1st month free” to users who already subscribe to creators on other platforms.

- Daylight verifies data from utilities to validate local energy prices and electricity usage.

- Heale verifies data from logistics SaaS platforms to determine settlement of deliveries.

Walled gardens are a defining feature of web2 economics. Under the guise of “data as a moat”, a generation of investors learned to bid up platforms whose only moat is access to proprietary reputation graphs up to 30-50x earnings multiples—collectively in the trillions of dollars. In a post-zkTLS world where platforms cannot expose data to users without also exposing it to third-party developers, these “platforms” are worth single-digit multiples of earnings. They are simply not defensible unless paired with some other moat. Opacity takes web2’s walled gardens and gives every user an infinitely-tall ladder in their pocket to take their data (and its associated value) across ecosystems freely. In the process, trillions of dollars of value will shift from these web2 into web3 networks who use reputation graphs to build other moats.

To learn more about Opacity, check out our research on zkTLS or listen to their talk at DePIN Summit. If you have portfolio companies that would like to integrate zkTLS for their own use case, please reach out.

Free Market is building Zapier for Web3 protocols, creating extremely easy and monetizable calls-to-action in structured formats. The company works directly with DeFi and DePIN projects to automate multi-step blockchain processes. Today, FM serves emerging protocols like Renzo, generating ARR from a small number of sticky clients. Longer term, they see a path to enterprise, and are currently in the early stage of engaging with large companies like Robinhood to create custom crypto integrations for their apps. We invested in Free Market’s pre-seed round alongside Longhash Capital and OrangeDAO.

We deployed to three new seed bets at a blended average entry valuation of and initial ownership of . With private markets running hotter than we’d like, our new investments this quarter were primarily founder-led decisions to back entrepreneurs that we felt we couldn’t afford not to back, with ambitions to create category-leading networks in novel sectors of DePIN. Axal is building infrastructure for autonomous agents. Axal’s founder, Ash Ahmed, started Axal from his dorm room at Harvard University earlier this year. He is one of the sharpest young engineers we’ve ever met, with a compelling vision for how verifiable autonomous agents will interact with onchain economies. Since our investments in Bittensor and Autonolas last year, we’ve been closely monitoring the growth in onchain agent ecosystems and believe there’s a massive design space. Over the coming months, the Axal team is working on piloting their autonomous agent infrastructure with a handful of DeFi and DePIN use cases. We invested in Axal’s seed round alongside CMT Digital, Trident Digital and Maven 11.

Meshmap is building a 3D map of the world. Meshmap’s founder, Ryan Rzepecki, previously founded the bike-sharing company JUMP and scaled it to 12k+ bikes across 40 cities. After selling the business to Uber for $200m in 2018, Ryan founded a development studio focused on augmented reality. While spending millions of dollars of his own capital building AR apps, he had the insight that would lead to founding MeshMap: though most of the AR developer stack would eventually be commoditized, owning the mapping substrate on which AR developers collaborate is extremely valuable and defensible. MeshMap will use DePIN to incentivize users and developers to come to consensus on a global ground- truth 3D map of the world. Over the coming months, the MeshMap team will be working with select local partners to bootstrap maps in NYC, Tokyo and San Juan, showcased by their AR game City Champ. We invested in Meshmap’s seed round alongside a16z CSX, Colosseum, Lattice, GSR and notable angels.

Chakra is building a decentralized data warehouse and community-owned data marketplace. Chakra’s founder, Nirmal Krishnan, was previously the Head of Engineering at Artemis, a crypto data and analytics provider. At Artemis, over 1/3rd of total spend went towards database infrastructure vendors (Snowflake), consistent with our experience building DePIN.Ninja. By enabling data businesses like us to mix-and- match our own servers with on-demand resources from a distributed network, Chakra aims to deliver a more performant and cost-efficient database hosting, while also enabling new avenues for monetization via an opt-in data marketplace. Over the coming months, the Chakra team will be piloting their solution with several tier-1 crypto data businesses and traditional long/short hedge funds. We invested in Chakra’s seed round alongside Castle Island Ventures, Modular Capital, Race Capital and Hash3.

In addition to participating directly in venture deals, we sometimes look to gain exposure to early-stage projects as miners or validators. We recently made our first such investment into Glow, a protocol that incentivizes the buildout of solar energy deployments in high-impact locations. Glow is pioneering the market for solar-based carbon credits, which have historically been excluded from accreditation methodologies due to the challenges associated with measuring additionality (i.e., many solar farms are independently profitable before carbon credit subsidies). Through a clever onchain incentive mechanism, Glow makes crypto-economic guarantees about the additionality of the solar farms on its network, and monetizes by auctioning off the carbon credits generated by those farms. Glow’s founder, David Vorick, previously founded one of the earliest decentralized storage protocols, Sia. Fund I financed one of the first 25 solar farms on Glow, which for a few days was the highest-earning farm on the entire network. We believe the risk/return profile for early miners is materially better than investing in Glow’s private rounds.

Liquid Markets

In Q3, Helium (HNT) and Bittensor (TAO) ranked #1 and #3 top-performing among the top-200 crypto-assets by market cap, as sentiment began to shift from dispersion into consolidation of attention, capital and talent behind category-leading projects.

While our quarterly reporting cadence lends itself to talking about quarterly returns, the fundamentals driving outperformance were put in place over a year ago. From our Q4’23 partner letter:

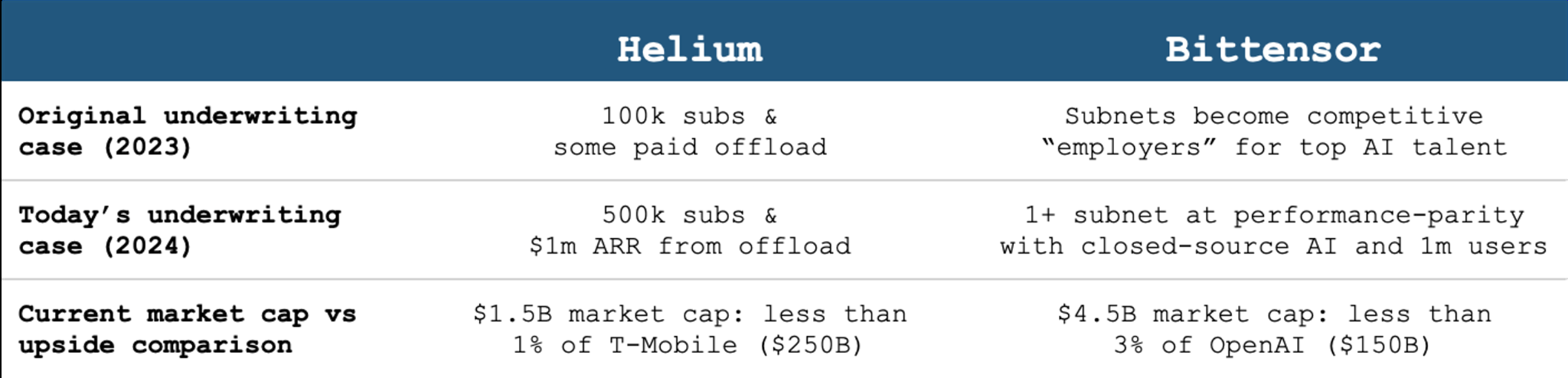

“We’ve been ideologically long Helium since the launch of EV3 almost two years ago (with $HNT trading above $20) but didn’t start building a position until Nov’23 at a ~$2.50 cost basis. By then, the key questions around Helium’s renaissance had been de-risked: Helium Mobile had already shown evidence of consumer virality in Miami (>5k subscribers paying $5/mo), the network was already offloading data via carrier-grade WiFi (which carries far less technical risk than CBRS), and the timing for the nationwide rollout was being openly discussed on monthly community calls. As the crypto-MVNO flywheel gains steam in markets across the US, we think Helium has a lot more room to run.”

“By Q3’23, discussions with leading miners in the ecosystem caused us to refresh our estimates to >$30m in cumulative training spend. More importantly, we saw miners aggressively hiring AI developers ahead of an upcoming network upgrade that would enable the creation of permissionless (and potentially highly lucrative) subnets on top of Bittensor. We doubled down on $TAO in Sep/Oct at a ~$65 cost basis, concurrent with the Revolution upgrade and the first third-party products going live. Today, there are 32 subnets building unique AI products on Bittensor. As the number and caliber of AI developers in the ecosystem continues to skyrocket, we believe Bittensor has the potential to be one of the most important permissionless networks on earth.”

Both theses are playing out as predicted, jump-starting the flywheel of upward reflexivity that makes us as excited about owning these networks today as we were back then. Across the two projects’ treasuries, the value of tokens allocated for future mining incentives increased by >$1.5B in Q3. Over the next eighteen months, we believe Helium will grow to 500k-1m subscribers plus $1-2m of annualized revenue from telco offload, and believe several Bittensor subnet apps will reach performance- parity with closed-source AI. At a scale of millions of users and with the power of token network effects behind them, these networks will look and feel like viable competitors to T-Mobile and OpenAI and will re-price from 1-3% of the market cap of their respective incumbents up to 10-20% or more.

While we have a constructive, non-consensus view on growth of these networks in the near-term, we think both networks will still have ambiguous unit economics for at least the next 18 months. Helium Mobile, even at a scale of 500k subscribers, will at best break-even on gross margins after paying T-Mobile $2-3 for every GB of subscriber traffic outside the range of a Helium hotspot. The first subnets to see mass adoption on Bittensor will likely be free, pushing the question of monetization to 2026. We are spending the time now to deeply understand the unit economics and path to profitability for each of these networks, so that we are a step ahead of the market again when these questions arise in ‘26-’27.

More broadly, this timeline aligns with the current state and future evolution of DePIN capital markets. When we raised Fund I in 2022, a handful of projects like Filecoin, Helium IoT and Dimo had proven out DePIN’s ability to finance and coordinate the global buildout of infrastructure networks. Private markets investors were focused on the “scalability” of supply-side (i.e., the cost and work required to deploy nodes) and public markets focused on forward expectations of active node growth. We used to talk about valuing DePINs based on a book value multiples of their connected hardware. From 2022 to 2023, the number of DePINs with thousands of active nodes increased from a few to a few dozen.

Today, a handful of projects have proven out DePIN’s ability to generate organic demand for products that are better or cheaper than web2 alternatives. Helium handles offload traffic for 3 of the 4 biggest telcos. Hivemapper maps roads for 3 of the top 10 biggest mapping companies. Geodnet’s high-precision positioning serves farmers through a partnership with the US Department of Agriculture. Combined, the three networks have burned >$2m worth of tokens from demand-side revenues. Today, private markets investors are focused almost entirely on demand-side potential, and public markets value networks based on forward multiples of onchain revenue. From 2024 to 2025, we think the number of DePINs generating millions of dollars of demand-side revenue will increase from a few to a few dozen (currently 8).

In 2026 to 2027, towards the beginning of Fund I’s realization period, the market’s focus will shift from demand to profitability. Networks with the ability to generate strong returns on invested capital, especially those in large end-markets that can continuously re-invest into compounding growth, will be awarded premium multiples by the capital markets. We’ve held our investments to this bar since 2022, which has often led us to pass on deals where other investors get excited about the near-term supply-side or demand-side potential but haven’t dug deep enough to understand the unit economics. At EV3, our focus has always been on maximizing our funds’ long-term ownership of the highest-quality networks.

The current sentiment across the crypto industry is best described as a pregnant pause: amid a myriad of tailwinds we could’ve only dreamed about years ago - central banks slashing interest rates, Wall Street opening the gates to regulated crypto investment products, and politicians launching their own tokens - folks who had conviction to stick around through ‘22-’24 are near-uniformly bullish heading into Q4. At the same time, the “centralized exchange listing window” has closed and put many people’s plans on hold: there were zero major DePIN token launches on centralized exchanges in Q3 (the most high-profile launch - Peaq, which raised $20m in public sales earlier this year - had its listing delayed into October). Without high-profile new listings to steal mindshare, the venture-backed DePINs with concentrated insider ownership that underperformed in Q2 were relatively immune to outflows in Q3. We expect this to change dramatically in Q4 as the listing window re-opens and several category-leading projects launch long-awaited tokens (Eigenlayer in restaking, Andrena in fixed wireless, Daylight in energy). We believe Q4 will see the widest dispersion of DePIN returns in the liquid markets since we launched EV3 as capital, attention and talent continues consolidating into the highest-quality networks.

Closing

With macro tailwinds and the listing window reopening, we anticipate wide dispersion in Q4 returns as capital and talent continue concentrating into high-quality networks. As always, thank you for your continued support.

Your partners,

Sal & Mahesh