Market Update

If there’s a single word to describe the state of crypto markets, it’s dispersion— of capital, talent and attention. Nearly a quarter of all tradable onchain assets - and a quarter of all active DePIN projects - were created in the past six months. Venture firms are backing the nth competitor in a category at seed-stage, rather than paying up to own the category-leader at a nine/ten-figure market cap liquid. Individual investors are spinning out from larger firms en masse to write smaller, earlier checks. Protocols are rolling-their-own blockchains in an attempt to re-rate to “infrastructure multiples”, rather than use cheap blockspace from the deluge of new general-purpose L1/L2s. There are huge incentives to launch something—regardless of what it is.

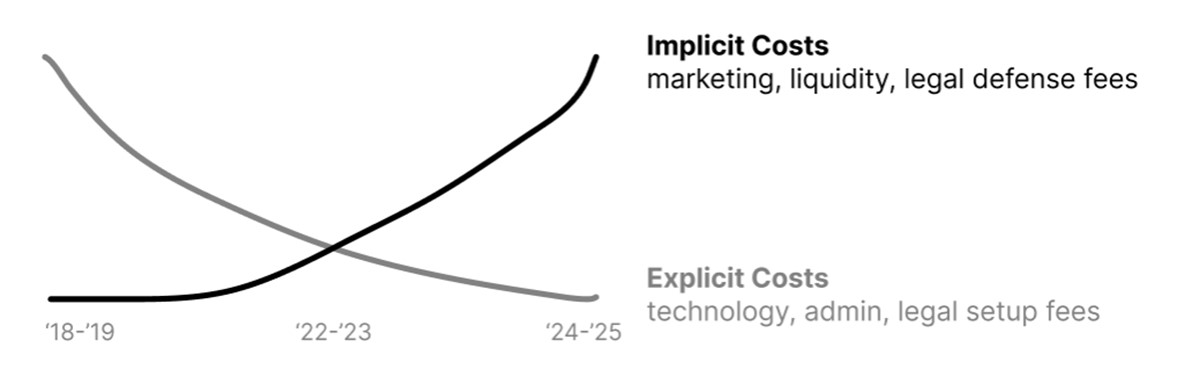

While the up-front cost required to launch a token/chain/fund has never been lower, the implicit costs of reaching critical mass have never been higher. To reach true minimum viable scale today, crypto entrepreneurs and GPs need to both attract enough attention and/or liquidity to cut through noisy crypto markets, and also be sufficiently conservatively-run and/or well-capitalized to navigate an uncertain regulatory landscape.

The two costs were roughly equal when we raised Fund I. Today, implicit costs are an order of magnitude higher, but the market hasn’t realized it yet. Entrepreneurs raising seed rounds today are not budgeting for the costs ($2-3m) and dilution (5-10%) required to get a token listed on several top exchanges with deep liquidity. Similarly, the investors participating in them are not budgeting for traditional venture-like loss ratios on their capital; if a project fails, they figure they can recover their principal by selling into liquid markets. Over time, it’ll become clear that - while there’s no technology hurdle to operating a <$10m venture fund or <$50m FDV protocol - the minimum viable scale for managing real-world relationships with critical centralized counterparties (i.e., exchanges and regulators) is at least 5-10x higher. In other words, the idiosyncratic terminal risk inherent in new ventures - especially in a nascent, volatile industry like crypto - is being mispriced by capital allocators because of the perception of liquidity: naive GPs conflate paper marks with real outperformance, while naive LPs conflate great investors with great investment firms with durable competitive advantages.

Our Q1 market outlook, re-printed below, has proven correct so far. In private markets, the highest-quality DePINs both inside and outside our portfolio raised several years’ worth of runway in the first half of the year. In liquid markets, tokens within upcoming unlocks were the quarter’s worst performers, as insiders took profits that pushed price down from a 9x unrealized MOIC (based on insiders’ estimated cost basis) to 5x on a median basis.

After every period of dispersion comes a period of consolidation. As the market digests the fully-loaded costs of operating a crypto business, the dominant strategy shifts from optimizing for speed (“launch token as quickly as possible”) to optimizing for defensibility (“launch token as soon as you hit critical mass”). We’ve been investing behind this insight since early 2023, when we made three investments - Andrena in fixed internet, Daylight in energy, and Nosh in food delivery - that are expected to launch networks in 2024 generating seven-figure onchain ARR on day one. Assuming a median multiple (55x) and early float (15%), as a rule of thumb we expect every $1m of onchain ARR to support $350m of fully-diluted value at launch.

We expect a wave of mergers, acquisitions and partnerships to drive capital, talent and attention back to category-leading networks with emerging moats. DePIN 1.0 leaders like Helium, Bittensor and Filecoin are all approaching similar end-game architectures congruent with this worldview with HIP-51, Revolution and Interplanetary Consensus, respectively. While implementation details differ, each protocol upgrade implements a form of Crypto-Federalism where the ecosystem’s native token backs a set of competing subnets or subDAOs, each with its own semi-independent economics and governance. In web2 parlance,these DePINs are maturing into platforms that leverage their global communities, robust governance, and deep token liquidity to execute on multiple bets in parallel. As consolidation pressures build, more and more early-stage founders will view these crypto-federalist platforms as a better risk-adjusted path than bootstrapping an entirely new ecosystem from scratch. As technology investors, we have to pay close attention when we see new platforms emerging .

“A product is useless without a platform, or more precisely and accurately, a platform-less product will always be replaced by an equivalent platformized product.” — Steve Yegge

Portfolio Update

We deployed into private deals in Q2: across three core seed-stage investments - Raad, Spot and Prophetic

Raad is a decentralized weather data collection network incubated alongside our friends at Montauk Climate, CoinFund and Tribe. Most weather data today is collected by non-profits or governments and made available for free. While this works for 80% of use cases, poor data quality and static collection processes makes it unsuitable for the highest-value use cases. Raad is focused on serving the most lucrative cohort of weather data buyers - financial institutions - with a value prop that doesn’t exist anywhere else: institutional-grade local weather data on-demand. The 10 other projects in the space are led by community-builders or hardware manufacturers, not data experts. Our partners at Montauk have been purchasing weather data at scale for over a decade as Head of Venture at a $40B AUM energy PE firm and Head of ESG at a $15B hedge fund. With Montauk’s insights on scaling institutional demand for weather data, combined with our insights on scaling DePIN supply, the goal is to bootstrap the world’s largest and most robust weather forecasting network over the next few years.

Prophetic is developing a non-invasive neuromodulation device designed to induce lucid dreams and other conscious experiences—perhaps our most ambitious bet yet. Prophetic’s master plan is deceptively simple: 1) develop a mass-market device that safely induces lucid dreams, 2) overlay a communications protocol that allows users to communicate over IP while dreaming, and 3) create a metaverse where users collaborate with each other across various states of consciousness. Prophetic’s founder, Eric Wollberg, was the first employee at Praxis, and is exactly the type of maniacal leader needed to bring such a far-fetched vision into reality. The company is working with leading researchers at the Donders Institute to develop its headset prototype; if you’re in NYC and would like a demo, please reach out. We’re excited to back Eric and the Prophetic team in their pre-seed round led by our friends at BoxGroup.

Spot is a decentralized exchange for long-tail assets starting with memecoins for celebrity athletes. While most institutions see memecoins as the bellwether sign of crypto’s speculative excess, we believe they are here to stay: memecoins allow issuers to monetize attention faster than ever before, with ~zero fixed costs and ~zero platform risk. The internet created a cohort of attention-rich, cash-poor celebrities for whom memecoins are the most compelling way to monetize their public persona. Spot is building an exchange for non-crypto-native audiences that makes it extremely easy to launch and trade celebrity memecoins - and in the future, any cryptoasset - while abstracting away onchain complexity. To everyday fans, Spot is an in-app personal assistant that seamlessly executes trades. We’ve had the privilege of working with Spot’s founder, Nicky Montana, as a co-investor in several EV3 portcos through ZK Ventures and are excited to participate in Spot’s pre-seed round alongside notable angels.

We built one new core position in the liquid markets during the quarter: MOBILE. The Fund has owned Helium’s native ecosystem token - HNT - since Q4’23, when we began to see signs of viral growth in Helium Mobile’s $20/mo nationwide unlimited cell phone plan. At the time, we viewed HNT as the primary conduit for value accrual in the Helium ecosystem, with economics tied directly to network-wide bandwidth usage via the burn-mint-equilibrium.

Earlier this year, we began to notice a change in attitude, where HNT’s exclusive claim on data transfer economics - previously a sacred tenet of the community - began to erode. Historically, recurring (high-quality) data transfer fees accrued to HNT and one-time (low-quality) onboarding fees accrued to subDAOs. However, as MOBILE’s speculative premium over its redemption value declined from 50x to 10x, and as quarterly new subscribers declined from >50k to <25k in Q2, the community accepted the need to shift value from HNT to MOBILE. Our view was confirmed in a podcast we recorded with Nova Labs’ GM of Wireless, at minute 37:

Sal: “If you could make whatever changes you wanted to the Helium DAO for a day without community approval, what changes would you make to set things on the right track?” Boris: “If I had a magic wand, I would get rid of the IOT token and I would leave HNT+IOT as one token focused on IoT. And then, I would have a completely different token for cellular networks that has its own burn economics… I would do away with programmatic treasury, the three-token system, and HNT as a backing for subDAO tokens.”

For subDAOs to be a viable model, Helium must alleviate the tax charged by the parent DAO, which is currently a 100% tax on all data transfer economics. MOBILE trades at less than half the market cap of HNT, yet most HNT holders attribute value primarily to the success or failure of Helium Mobile. As the market realizes the inevitability of value leakage from HNT to MOBILE, the latter will benefit from both intra-ecosystem flows - i.e., HNT holders repositioning to MOBILE - and inter-ecosystem flows - i.e. investors making net new bets on Helium Mobile, now that there’s no dilution from the legacy IoT network. With both tailwinds in play, we see asymmetric upside in MOBILE and built a position following the public release of our podcast.

As value is pushed further towards the subDAOs, Helium will need to accelerate both the number and breadth of subDAOs in order to realize the network-of-networks vision and grow into its upside potential for HNT. The process is underway, with the first energy-focused subDAO announced a few days ago on our podcast. By the end of this year, it’ll be clear whether Helium is on track towards creating a sustainable ecosystem of subDAOs unified around HNT. In the failure case, Helium risks suffering a similar fate to the Cosmos Hub, which - despite an early technology advantage and strong community - has not been able to create a flywheel where more usage begets more value for the ATOM token, and vice-versa. We are closely monitoring both onchain activity and community sentiment as we re-underwrite our HNT thesis in the light of the new developments.

Separately, we built positions in BTC, ETH, and SOL that we plan to recycle in 2024-2025.

“When the facts change, I change my mind. What do you do?” — John Maynard Keynes

Firm Update

Building a great fund is one thing; building a great firm is another. Since launching EV3, we’ve defined ourselves as DePIN’s investor-builders with a simple strategy: raise DePIN- focused investment funds, invest in leading DePIN projects, and re-invest our management fees into public goods that accelerate the DePIN ecosystem and drive excess returns for our funds.

With a full-time team of three, we’ve helped solidify DePIN at the forefront of crypto by launching the leading DePIN podcast, newsletter, conference and analytics. As a result, DePIN has grown from 2-3% to 8-10% of crypto mindshare as measured by both alts market cap and conference side-events. .

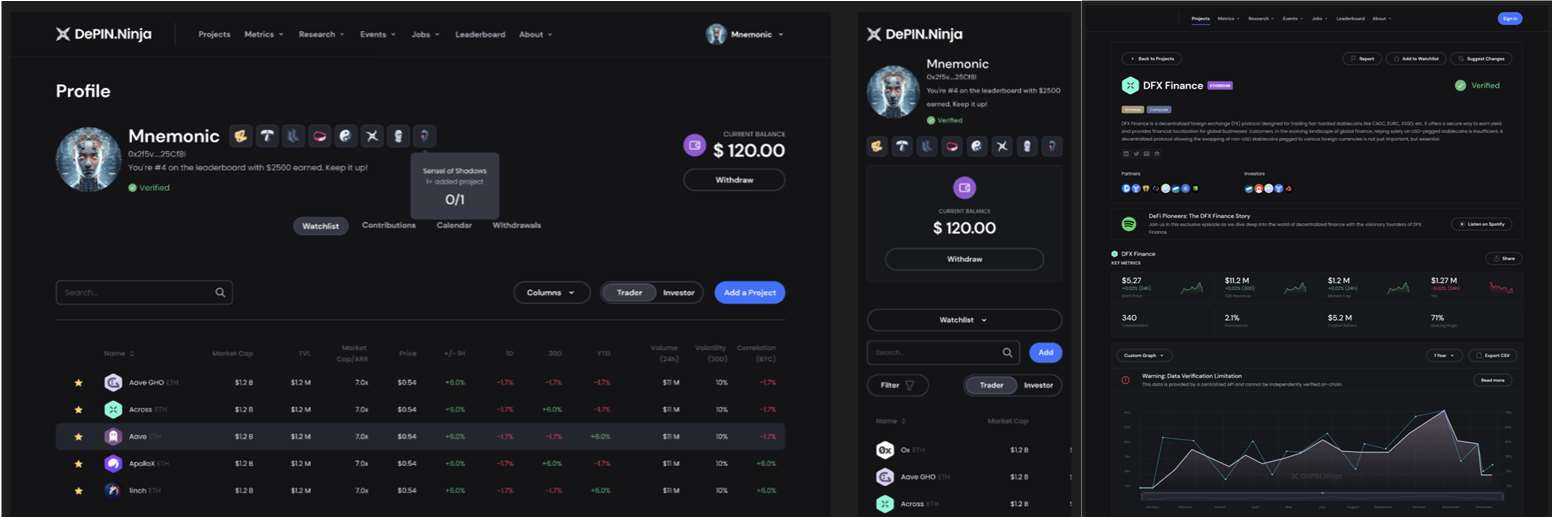

We’re launching a new version of DePIN.Ninja, our community-powered sourcing machine. The new release will incentivize users with crypto payouts for submitting new DePIN projects to our open-source database, plus a potential share of carry economics if EV3 ends up investing. Behind the scenes, our human+AI analysts verify submissions to maintain a high-quality database. The process is entirely transparent, built on public repos and onchain payments logic.

We’re formalizing our research efforts with EV3 Research, a new initiative focused on producing and distributing institutional-grade DePIN research. We recruited Vinayak Kurup to lead the efforts and published our first piece in June. There’s a massive unexplored design space around taking advancements from the broader crypto ecosystem and applying them to DePIN. Opacity is doing this for zkTLS, including enabling our other portcos Daisy, Nosh and Unofficial to securely access user data from incumbent web2 platforms like TikTok, Doordash and Spotify. Infrastructure protocols like Opacity need to first achieve product-market fit with developers, who in turn build apps to achieve product-market fit with users. Most protocols get stuck in the first phase, unable to create awareness to attract a critical mass of developers. With EV3 Research, we’re creating a machine to bootstrap early developer ecosystems by drawing attention and capital to the emerging primitives in DePIN and Web3.

We’re excited to have Brandon Leppke, our new Head of Operations, joining us full-time from Cole-Frieman & Mallon LLP. Brandon has been part of the EV3 story from the beginning, helping to spin up our management company, first venture fund, and now . As we scale to multiple funds and invest more aggressively into our technology, media and research, Brandon will architect and institutionalize the operational and legal processes behind it all.

As we expand the team beyond the two of us, we’ve begun to define the core principles behind the culture that makes EV3 different from other investment firms.

- We operate with an extreme degree of individual ownership.

- We have a bias for action and bet big on our highest-conviction ideas.

- We play long-term games with long-term partners. We expect the folks we recruit to live these principles every day the same way we do. True to the first principle, every part of the EV3 platform is led by a single owner: Steen leads DePIN Summit, Vinny leads EV3 Research, Mahesh leads Proof of Coverage, Sal leads DePIN.Ninja, DePIN Snacks and State of DePIN, and Brandon leads operations and legal for all of the above. Ruthlessly delegating ownership allows Mahesh and I to focus on what we do best: making high-quality investment decisions and solving critical problems for our portfolio companies.

The next phase of EV3 is about architecting a team and culture that’s capable of capitalizing on our unique view of the future - the inevitability of DePIN - to generate exceptional returns by creating durable advantages powered by open-source technology, media and research. We are forever grateful to you, our partners, who trusted us in 2022 at a time when the future of crypto - and certainly DePIN - was in doubt, to turn our vision for EV3 into a reality. “There is no ‘product’ in your future company beyond your ability to make decisions. That makes good hiring crucial: the people around you will either protect or infringe on the climate within your skull.” — Graham Duncan

Predictions

In our Q4’23 investor letter six months ago, we made the following predictions for YE’2024:

- L1 Wars: More DePINs will be built on general-purpose L1s (Solana) and L2s (Base) in 2024 than on DePIN-specific L1s (IoTex) and app rollups (Caldera). Status: on track. There are now more than 40+ venture-backed DePIN projects on Solana.

- DeWi Resurgence: Helium reaches 150k+ cellular subscribers and a new fixed wireless network (Andrena or Althea) gets bid up to $1B+ FDV. Status: on track. Helium grew from 20k to 100k subs in the first half of the year. Andrena’s growth is accelerating.

- Compute Dominance: Compute will continue to be the biggest category of DePIN by both revenues and market cap at the end of the year. Status: on track. Compute has actually increased market share this year with the rise of decentralized GPU clouds.

- Mapping Users: Mapping will be the single biggest top-of-funnel for non-crypto native users, with 1m+ users earning a mapping token as their first crypto. Status: too early. Natix & Hivemapper have >275k combined contributors, but may not reach 1m this year.

- Onchain Security: Security Finance (SecFi) emerges as the third vertical of developer onchain tools - alongside oracles & RPCs - to reach a $1B market cap. Status: wrong. Novel devtools categories like zk-coprocessors are seeing faster adoption than SecFi.

For our supporters who made this far into the letter, here are five more falsifiable predictions for DePIN we expect to see in the second half of 2024:

- Platform Positioning: As DePIN 1.0 networks like Helium / Filecoin / Bittensor converge ‘networks-of-networks’ positioning, several mid-cap DePINs (sub-$1B FDV) follow suit, seeking to re-rate to platform-like valuations.

- Race for Medallions: Protocols with medallion-based staking (including Andrena and Daylight) collectively attract $250m+ of staked TVL and $100m+ of liquid staking TVL.

- zkTLS Everywhere: DePINs begin using zkTLS en masse to target token incentives towards long-term users and suppliers rather than airdrop farmers, leading a zkTLS infrastructure provider to raise at a $500m+ valuation in the private markets.

- Sora Summer: OpenAI publicly releases Sora, their new video generation model, spurring a host of competing open-source video-gen models, leading video-gen use cases to become the biggest driver of revenues for decentralized GPU networks.

- Energy Emergence: Energy grows from <5% to >10% of DePIN projects and market cap, with more than one energy DePIN reaching $1B+ FDV in the liquid markets.

Your partners,

Sal & Mahesh

Notes

Represents circulating DePIN market cap as a percentage of total crypto market cap less BTC, ETH, and stablecoins. Last quarter’s letter cited 2.2%, which included only the top 10 DePINs; on an apples-to-apples basis, dominance was flat at 9% in Q1 vs Q2. ↩

In past bull markets, quarterly active crypto developer growth peaked at 45% in Q3 2017 and 30% in Q1 2021. ↩