Market Overview

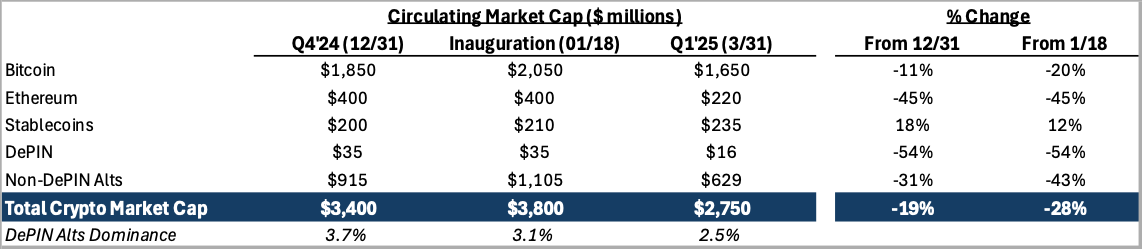

Crypto ended the quarter with $2.8T of market cap, down -18% QoQ as markets were forced to digest the bipolar impact of one of the most bullish events in crypto’s history (the inauguration of the first crypto-friendly US administration) no more than 48 hours after one of the most wealth-destructive events in crypto history (the launch of the $TRUMP and $MELANIA memecoins) by that very same administration.

Since then, crypto has faced a trifecta of flows-related headwinds: namely, a massive deceleration in ETF inflows (-98% QoQ), exacerbated by an acceleration in new cryptoasset launches (+80% QoQ) and insider vesting for existing cryptoassets (+46% QoQ). DePIN was hit especially hard, underperforming the broader crypto alts universe and ending the quarter with a $16B market cap (-54% QoQ). In our previous letter, we told you “investor optimism for DePIN… appears to be approaching exuberance”. The tides turn quickly in the crypto markets, and today this is no longer true: DePIN is once again non-consensus, with weak-handed holders and miners selling off their positions indiscriminately in Q1’2025.

With intra-crypto capital rotations becoming increasingly short-lived, the billion-dollar question in crypto is where the next wave of external flows will come from. Empirically, the biggest post-election winner has been $XRP, which added $120B+ of market cap and rose 400%+ as traders sought to front-run flows post President Trump hinting at its potential inclusion in a Strategic Reserve. So—who will bring the flows?

One view is inflows will come from TradFi allocators, in which case the 15+ cryptoassets with active ETF applications are likely to outperform. A second view is that retail speculators will re-enter crypto, driven by falling rates and mainstream fintechs like Robinhood deepening their crypto offerings. In this version of the world, a 2021-like market structure emerges whereby front-running listings is the dominant strategy: the meta-game becomes predicting which tokens the major fintech platforms are most likely to list first. Anecdotally, we’d estimate 80% of investors cite one of the above two reasons for being bullish on alts.

The third, and least popular, view is that protocols will generate sizable onchain revenues that drive organic demand for tokens via buybacks or dividends. Hyperliquid, whose native token $HYPE is up +100% since launching in late November, generates ~$1m/day in onchain trading fees and directs half that revenue (~$500k/day) towards token buybacks. $HYPE is valued at a 25x multiple to those buybacks on a circulating market cap basis (70x fully-diluted). Their success spurred DeFi protocols including Kaito, Jito, Aave, Jupiter and DYDX to implement similar buybacks shortly thereafter. Markets reacted positively to buybacks initially, with a +7% median intra-day move at announcement. However, since then many investors and influencers have criticized buybacks as being a return-insensitive use of capital (i.e. tokens) that could theoretically otherwise be used to incentivize further productive growth for the network.

Open vs. Closed Protocols

In our view, the story is more nuanced. The best capital allocation machines in history have concentrated investment decision-making into the hands of a small number of individuals. DAOs have historically been worse at capital allocation than even web2 startups. We have no reason to believe either trend will change anytime soon, but the issue of capital allocation depends on the nature of the network: open vs closed. For open protocols, or network tokens, programmatic buybacks are the best way to protect tokenholder interests; for closed protocols, or company-backed tokens, founding teams should have some ability to conduct discretionary token buybacks the same way CEOs conduct share buybacks.

This is a distinction we haven’t made before, so it’s worth double-clicking on what it means. Open protocols are valuable because they are open : because no single person or entity can control the network, developers can build on top of the protocol without worrying about platform dependency; in the words of Chris Dixon, open networks are built with steel, not wood. Closed networks, on the other hand, are valuable because they are closed: because a highly-credible and ambitious team at the helm of the network can execute and scale onchain revenues faster with unilateral control over the protocol.

Open Protocols We’ve come to view investing in open protocols as a fundamentally different category than closed protocols, with its own set of founder archetypes, protocol architectures, and return profiles. We continue to believe open protocols are the biggest and most asymmetric investment opportunities on earth today, giving the world’s most ambitious founders the tools to harness reflexivity and drive 100x+ type outcomes. Like Bitcoin, these protocols seek to create an economic system that scales to the level of nation states. Indeed, many of the founders building open protocols are heavily inspired by Bitcoin, evident for example in Bittensor’s inflation schedule and Glow’s proof-of-work mechanism.

For open protocols, community-market fit (CMF) typically precedes product-market fit (PMF). While it can take several iterations or years to show the traditional signs of the latter (revenue, retention, users), the former is often visible from the earliest days of a network. Protocols with CMF are rare, but we have found they have a few defining characteristics: 1) an unusually-rabid community with an unusually-low time preference, 2) an uncanny ability to bounce back from major setbacks even stronger than before, and 3) a focus on creating an immutable, permissionless protocol that puts everybody on equal footing.

The challenge with investing in new open protocols is their tendency for low liquidity and high volatility. Open protocols don’t engage with the token industrial complex, i.e. the exchanges, market makers, influencers, advisors that demand up to 5-10% of networks to secure retail attention and exit liquidity, and as a result they can be difficult to trade and custody—just like the early days of BTC. For example, Bittensor wasn’t supported by Ledger custody or Binance exchange until after it hit a $3B market cap. Unlike closed protocols, the upside for open protocols disrupting markets as large as money, intelligence, energy, and governance is so high that selling only makes sense if you no longer believe the network has a path to becoming the n-of-1 leader in its category. Bitcoin’s critics have infamously called the top on the “valueless” network in 2016 at $10B market cap, in 2017 at $100B, in 2021 at $1T, and before long they will have the opportunity to make the mistake again at a $10T market cap. Inevitably, the market for sovereign money is so large and Bitcoin’s provenance is so unique that it has become the single best-performing asset of the past decade. Given the scale of the upside, the right question to ask is: what mental framework would have given us conviction to hold BTC through a 300x gain over the past decade, without selling through the Gox hack, block size wars, China ban, ICO mania, Operation Chokepoint…?

We’ve shared research on Bittensor and Glow in prior letters. Our newest open protocol investment is MetaDAO, a protocol pioneering a market-based governance model called Futarchy. MetaDAO works by creating two conditional tokens that are redeemable when a certain condition is met (or not). Users must lock collateral to mint these conditional tokens, and the conditional tokens are tradeable on exchanges. If after a period of time the redeem-upon-yes token trades higher than redeem-upon-no token, then the market believes the underlying collateral is more valuable in the yes case, and vice-versa. MetaDAO’s protocol is fully generalizable: the architecture is unopinionated about the specific condition considered.

MetaDAO was launched a year ago by a pseudonymous team at Solana’s MtnDAO accelerator. Their first product, a governance tool for DAOs, puts governance proposals up for vote via futarchy rather than the traditional token- or stake-weighted voting. More recently, MetaDAO announced a token launchpad for creating new tokens natively powered by futarchy-based governance. Launchpads, led by Pump.Fun and Virtuals, are among the most profitable businesses in crypto this cycle. The first MetaDAO-powered token launched earlier this week (Apr 2nd) and raised $200k in two hours. The $META token itself has a market cap of less than $30m today and no programmatic inflation: instead, inflation is determined by futarchy- based governance proposals which make future circulating supply highly uncertain & reflexive. MetaDAO is pioneering an entirely new type of market and we expect the protocol will go through natural growing pains as its market cap rises and its treasury becomes a target for adversarial governance attacks.

Closed Protocols

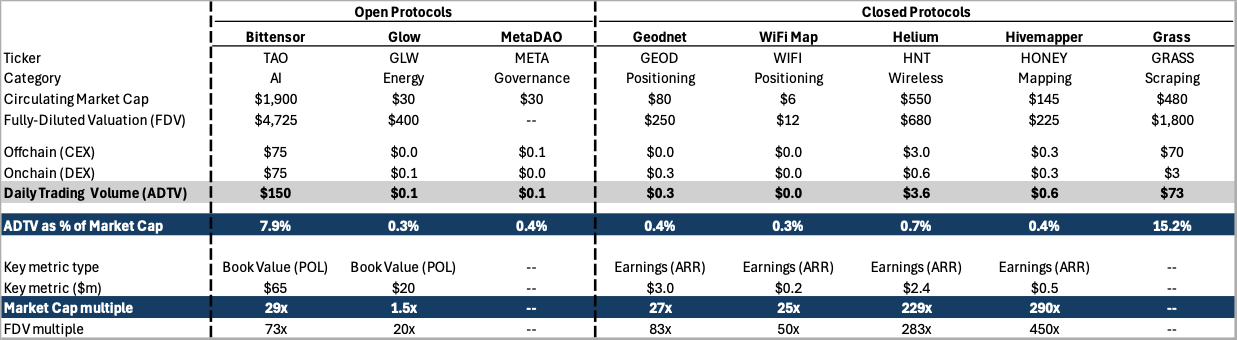

Closed protocol tokens are effectively junk equity: a framework we first wrote about in 2022. Token- holders have a junior or subordinate claim on network economics relative to company shareholders. Shareholders can choose to give a portion of their cash flows to tokenholders—or they can choose not to. You might expect these junior claims to trade at a discount, but empirically the opposite is true: for any given network, the token is typically valued at several multiples of the associated company’s equity value.

Closed DePINs today trade anywhere from a 25-30x multiple ($GEOD and $WIFI) to a 200-300x multiple ($HNT and $HONEY).2 The former are actually growing faster than the latter, despite the lower run-rate multiples. The “blue chip premium” appears to be associated primarily with being listed on tier-1 exchanges like Coinbase, Bitget, or Bybit. While retail speculators contribute relatively small amounts of trading volumes, they are evidently willing to pay much higher multiples than crypto-native traders.

Ask three crypto VCs how much revenue DePINs are generating and you’ll get five different answers. The lack of transparency and standardization across the space makes benchmarking difficult. As a result, valuation multiples vary so widely they’re effectively useless. Take decentralized GPU clouds for example: Aethir ($ATH) trades at 2x onchain revenues while Render ($RENDER) trades at nearly 1,000x, and both are in the same core business of aggregating, orchestrating and reselling GPU capacity. 2 To be clear, these multiple only count the (net) onchain revenues that are shared with the network.

DePIN Revenue Landscape (Q1'25)

To give a brief - some might say blunt - overview of the current DePIN revenue landscape, there are eight protocols generating ~$200m ARR collectively valued at $10B FDV, implying a ~50x multiple. However, these protocols’ revenues are not directly tied to tokenholder value accrual:

- Aethir ($ATH: $1.3B FDV) generates >$100m onchain ARR, however the majority appears to be affiliated with company insiders and therefore does not result in net buy pressure on the token.3

- Grass ($GRASS: $1.8B FDV) is privately reporting “mid-eight figure” revenues, however this hasn’t been made public and there is no (publicly-announced) plan to move revenues onchain.4

- IO.Net ($IO: $0.6B FDV) generates >$20m offchain ARR, however this is self-reported and the IO.Net team has been in the process of “migrating” the revenue onchain for at least two months.

- Glow ($GLW: $0.4B FDV) generates >$20m onchain revenues, however this is from one-time staking deposits that miners expect to recover and doesn’t directly drive net buy pressure.

- Akash ($AKT: $0.3B FDV) generates >$4m onchain ARR, however this represents the gross revenues earned by miners for compute jobs and does not drive net token buy pressure today.5

- Filecoin ($FIL: $5.5B FDV) generates >2m onchain ARR, however the majority of this revenue is generated from slashing penalties and batch fees unrelated to paid demand for data storage.

- Hivemapper ($HONEY: $0.2B FDV) generates >$0.5m onchain ARR, however the growth is extremely spiky (-85% QoQ in Q1’2025) and decoupled from their reported customer growth.6

- Livepeer ($LPT: $0.2B FDV) generates >$0.5m onchain ARR, however this represents the gross revenues earned by miners for compute jobs and does not drive net token buy pressure today.

Separately, there are five protocols generating onchain revenues that directly benefit tokenholders through a buyback and/or burn mechanism. Collectively, these networks generate ~$10m of annualized buybacks and are valued at $1B fully-diluted, implying a ~100x multiple. Because customers access the network via a centralized intermediary, tokenholders in closed protocols must trust insiders to distribute a “fair” share of economics back to the network. Some protocols, like Geodnet, commit to using a fixed percentage (85%) of offchain revenues for token buybacks. Others, like Helium, set a fixed price-per-unit ($0.50 per GB) that companies must burn to access the network’s capacity. The former is problematic because the denominator (i.e., offchain revenues) cannot be verified—it is impossible for tokenholders to enforce the “royalty”. The latter is problematic because insiders are incentivized to set prices as low as possible to maximize shareholder profits at the expense of tokenholders.

- Braintrust ($BTRST: $70m FDV) generates ~$3.3m onchain ARR via 15% revenue share.7

- Geodnet ($GEOD: $250m FDV) generates ~$3.0m onchain ARR via 85% revenue share.

- Helium ($HNT: $675m FDV) generates ~$2.4m onchain ARR via a $0.50 per GB fee.8

- Natix ($NATIX: $65m FDV) generates ~$0.7m onchain ARR, with no forward guidance.

- WiFi Map ($WIFI: $12m FDV) generates ~$0.4m onchain ARR, with no forward guidance.

A skeptic would look at today’s DePIN token universe and see two choices: pay ~50x for revenues you’re not sure exist today, or pay ~100x for revenues you’re not sure will exist tomorrow.9 We largely agree: 95% of DePIN tokens are overvalued… but the remaining 5% are massively undervalued. Our goal is to find assets in the latter bucket with both the potential to scale revenues by 10x+ over 2-3 years and the intention to direct a meaningful portion of those economics to tokenholders before shareholders.

Sal’s first office job was at a university endowment. Mahesh has been investing in funds for a decade. When we hear GPs underwriting 10x growth to justify 100x multiples, the hair on the back of our neck sticks up. Now that we’re in the GP seat, we want to provide our partners with the same explanation we would want: so, what’s driving our conviction to own DePIN tokens at the prices available in Q1’2025?

In short, because the highest-quality DePINs today are undervalued relative to both infrastructure REITs, at 20-30x earnings multiples with no growth, and also to L1 blockchains, at 1000x+ multiples with highly- volatile growth. As the pools of capital that own these assets today - yield-seeking infrastructure investors on one hand, and crypto-native speculators on the other - come to understand the uniquely asymmetric return profile of bringing real-world industries onchain, we believe capital will flow into the highest-quality DePINs as they become the consensus sector leaders of the digital infrastructure economy. The top five L1s and the top three telcos alone combine for >$1T of aggregate market cap vs DePIN’s mere $16B.

Valuation Framing

More specifically, we believe:

1. Onchain buybacks are comparable to EBITDA or free cash flow (bottom-line) multiples for equities rather than revenue or gross profit (top-line) multiples. Infrastructure REITs that own cell phone towers ($AMT, $CCI, $SBA) trade at 20-30x earnings in the public markets, as do REITs that own datacenters ($EQIX, $DLR) and renewable energy assets ($HASI). At current buyback multiples of ~100x, DePINs must scale revenues 300-400% to grow into the equivalent multiple.10

2. (Some) DePINs will carry a growth premium over and above traditional infrastructure. Even after 10x growth from today, DePINs will have captured less than 0.1% of their addressable markets in the US, and even less globally. Infrastructure REITs trade at 20-30x EBITDA with no growth opportunity; DePINs will trade at higher run-rate multiples given the growth premium. This is especially true for DePINs operating in the biggest end-markets (wireless, energy, compute).

3. (Some) DePINs will make tokenholders first-class citizens in the capital stack. REITs trade 20-30x earnings multiples because they 1) distribute 90% of taxable income to shareholders, and 2) have board members and auditors with a legal responsibility to defend shareholder interests. DePINs that put the interests of tokenholders above shareholders long-term, i.e. by setting key protocol parameters onchain (so they can’t be influenced by company insiders) have an arguably stronger claim on network economics than REIT shareholders do on company economics.

4. (Some) DePINs will re-rate to L2 (100-500x) or L1 (1000x+) blockchain-like multiples. L1/L2 tokens are valuable because validators can stake the token to capture MEV by manipulating the ordering of transactions on the chain. As successful DePINs launch appchains and/or settle more of their protocol-level economic activity onchain, the same will be true of DePIN. Whether by DePIN multiples growing and/or L1/L2 multiples shrinking, the valuation gap will eventually close.

9 One way to interpret the spread between a 50x and 100x multiple is that crypto markets give roughly half-credit for self-reported revenues that could benefit tokenholders sometime in the future vs revenues that drive tokenholder value today. 10 Some DePINs, like Geodnet, are currently growing revenues faster than that on a YoY basis.

TGE Environment

At Goldman, we both advised on IPOs and learned the process for seeding liquidity in the market for any given stock: gauging a company’s public market-readiness, preparing the S-1 and investor reporting, running the book-building and roadshow process, and managing price action at and post-launch. A good IPO advisor educates the market about a stock, estimates supply & demand to determine a launch price, and supports price stability by actively market making (“sales & trading”), sand-bagging projections (“beat & raise”), and flexing share supply (“greenshoe”). In crypto, these steps are often distorted or sometimes missing entirely, and as a result token launches (TGEs) tend to be more expensive, more volatile, and less likely to result in a positive outcome than IPOs. The truth is that virtually every role of an investment bank in an IPO process can and likely should be replicated in crypto—the non-risk taking aspects (marketing, book-building) by savvy founders and investors, and the risk-taking aspects (pricing, greenshoe) by leveraging DeFi protocols to eliminate the need for trusted/regulated intermediaries.

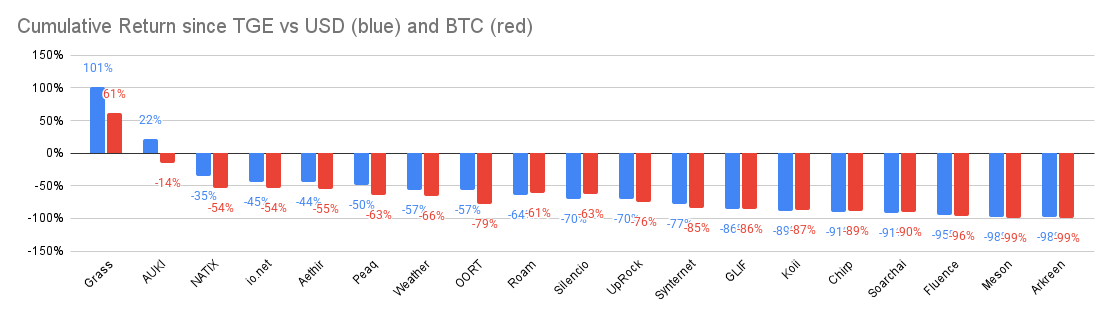

Recent liquid market performance for DePIN TGEs has been extremely challenging: of the 20 tokens launched since the beginning of 2024, only two have beaten USD and only one has beaten BTC. Almost half of these tokens are trading below $30m FDV - roughly where competitive seed rounds are getting priced today in the private markets - suggesting the market thinks they are no longer a going concern. While it can take patience to build a position in these tokens, the teams that survive and thrive will drive 10-100x returns from today’s prices.

DePIN TGEs since January 2024

11 Represents price return from each network’s TGE (token price after the first $500k of trading volume) to March 31, 2025.

Outro

We believe we are in a unique time in crypto where, more than ever before, the focus is on creating products with real utility and paying customers. This has been EV3’s focus since day-one, beginning with our 2022 thesis on decentralized wireless which has since expanded to include investments in decentralized energy, compute, mapping, logistics, identity, advertising and other large industries where crypto incentives can solve structural coordination challenges.

Many of you reading this were at one time, like ourselves, first-time entrepreneurs. One thing no one told us about being founders is that certain memories get seared into your brain in high-definition forever. May 2022 was one of those: we went into Friday thinking we had $10m soft-circled for our first close, and by Monday we had only $3m in the wake of Terra’s collapse. March 2023 was another: at 3PM Wednesday, we were driving around our parents’ neighborhoods, desperately looking for a bank who would open an account for us before the 4:30PM wire deadline—within two days our primary bank, SVB, was bankrupt.

But one of our most vivid memories together actually predates EV3. In 2017, we had just finished our summer internships at Goldman and were hanging out together in Sal’s shoebox apartment on the Lower East Side. We both had offers to join Goldman full-time, but after 10 consecutive weeks of sleeping 3-4 hours per night, the offers didn’t seem quite so enticing. Analyst programs are two years or 104 weeks: effectively ten, 10-week, back-to-back internships with no breaks in between… Were we ready to do that? We’ll never forget the grin on our faces when we turned to each other and laughed, because the answer was so immediately obvious to the both of us: there was 0% chance either of us was ever giving up.

After three years, before deciding to raise Fund II we had a similar discussion to that night back in 2017: are we really ready to pour everything we have into EV3, every day, back-to-back, for thirty years, with no breaks in between? The answer hasn’t changed, and neither have the grins.

Your partners,

Sal & Mahesh