Dear Partners

Dear Partners,

Crypto ended the quarter with $2.8T of market cap, up +50% YTD led by $12B of net inflows into spot Bitcoin ETFs. DePIN ended the quarter with $18B of market cap, up +100% YTD led by compute tokens becoming the consensus expression of the ‘AI picks & shovels’ thesis onchain. DePIN dominance, i.e. DePIN as a percentage of crypto market cap ex-BTC/ETH/stablecoins, rose from 1.6% to 2.2%. We expect to see this figure at 5%+ by year-end as roughly one-quarter of the 1000+ currently-active DePINs plans to launch a token in 2024.

A trio of factors, capital, technology and regulation, is driving the explosive growth in early-stage DePIN activity. There are now 15+ DePINs valued at $1B+ FDV that serve as favorable comps for venture investment committees. There is high-performance blockspace available across dozens of >100-TPS chains. Wyoming’s new law enables US-based entrepreneurs to compliantly launch decentralized organizations starting July 1st. The barriers to launching a DePIN have never been lower.

These factors are driving technologists from every corner of the globe towards experimenting with DePIN ideas. At the application layer, we’re seeing an acceleration of deal-flow in emergent categories like healthcare (smart rings & wristbands), energy (smart plugs & EV chargers) and logistics (sidewalk delivery robots & drone detection stations). At the infrastructure layer, we’re seeing experienced crypto builders adapt DeFi/L1 primitives like liquidity aggregation, off-chain data verification and shared security for DePIN. Since crypto VC returns have historically been concentrated in the latter category, top infrastructure-for-DePIN projects are often able to raise capital at 2-5x higher valuations and skip the pre-seed stage entirely. Fund I is invested primarily into the former category, where the business models are not yet well-understood by the current cohort of crypto investors. We will also make a handful of high-conviction bets in the latter category, where EV3 can catalyze growth via inter-portfolio partnerships.

Outside crypto, the cracks in centralized infrastructure continue to accelerate on a global scale. Take the wireless industry as an example: in February, AT&T’s nationwide outage left millions of Americans without internet for hours and even took down public safety (911) networks. In March, AT&T reset account passcodes for the 70m+ Americans whose data they leaked four years earlier. Outside the US, telcos in Taiwan, Malaysia, Paraguay, Australia, Israel, and Uganda disclosed major hacks in Q1’24 with many more likely going unreported. Without open-source, credibly-neutral infrastructure, events like these will continue to become more frequent and more damaging. DePIN is an inevitable global movement.

Across the six networks, our blended average entry price is below FDV and our blended average fully-diluted ownership is above . In other words, every ~$1B of FDV across them returns the Fund once over. For reference, there are 15 DePIN tokens currently valued above $1B FDV, including several Q1’24 launches like Fluence and Oort, and another 15 valued between $500m and $1B FDV.

Private Markets

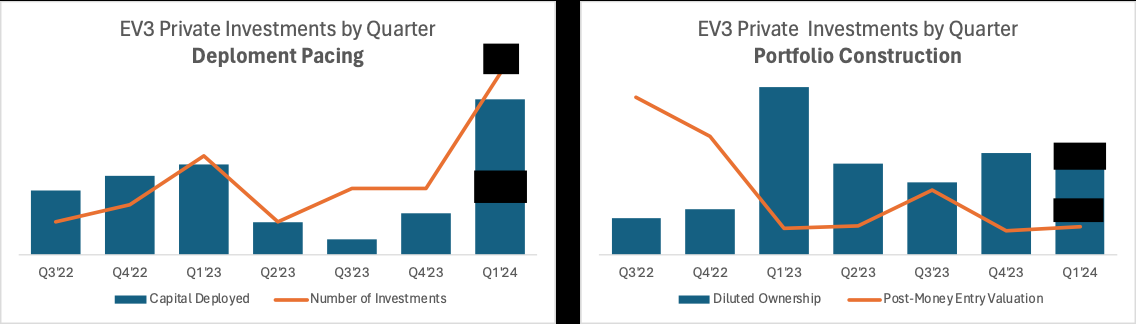

Q1’24 was our most active quarter ever in the private markets, both by number of deals ( ) and capital deployed ( ). Our conviction reflects the quality of DePIN founders at the pre-seed/seed stage, which is higher than ever. In addition to investing all of our available (called) cash, we took profits on certain liquid token positions, selling >$500m blended average FDV, to re-deploy capital into our highest-conviction private bets, buying <$25m blended average FDV.

For the past eighteen months, EV3 has been the marginal capital for DePIN pre-seed founders. If we passed on a DePIN idea, it probably wasn’t getting funded. Today, that’s no longer true: projects we pass on regularly go on to raise pre-seed/seed capital from other VCs, accelerators or L1s. Most multi-stage crypto VC firms have hired or designated a dedicated DePIN investment partner. Despite increased investor attention on the sector, the DePIN-focused analytics, media and events brand we built during the crypto bear market are now paying off and enabling us to scale capital deployment while maintaining discipline on entry prices and ownership targets.

As sector-focused early-stage VCs, there are three, really four, maneuvers by which to insulate expected returns as markets heat up: we can 1) invest in tier-1 founders that are overlooked by other investors, 2) invest in tier-1 founders before other investors get comfortable with a thesis or market, or 3) invest in tier-1 founders at the same time as everyone else but concentrate aggressively into only the very best companies. Alternatively, we can stop venture investing altogether and/or deploy into adjacent asset classes like liquid tokens or growth equity.

Path #1 drives the strongest moat: because founders will fight like hell for you if you believe in them when no one else does. Path #3 is the most scalable: because concentrating aggressively into illiquid assets can generate high cash-on-cash multiples on staggering amounts of capital. The middle path is both less scalable than the latter, i.e. limited by the number of tier-1 founders rather than portfolio concentration limits, and drives less moat than the former, i.e. more investors can reliably underwrite business models than reliably identify overlooked founders. Despite these tradeoffs, we believe the second path, backing exceptional founders before other investors can underwrite a thesis, is the right game for EV3 to play. While uncertainty is highest during this stage, it’s also when our accumulated insights and relationships within DePIN can have the biggest impact on fund returns.

The bulk of our capital during the quarter went to five new pre-seed investments, where we deployed at a blended average entry valuation of and ownership of :

1. Daisy is building a decentralized influence-sharing protocol that enables low-trust collaboration between influencers at scale. Influencers can get paid instantly for boosting each others’ paid social media campaigns with likes/comments/reposts. Brands can reach niche digital communities without encroaching on end-users’ privacy. Daisy leverages crypto infrastructure built by Opacity - another Fund I portfolio company - to serve ads based on social graphs at the influencer/community-level, rather than using cookies to track behavior at the individual user-level. This is the first-order correct way to structure an influencer ads market, and the imminent phase-out of Google’s third-party cookies in 2H’24 makes it an urgent problem for most brands. Daisy will operate in stealth for a few months while building out its platform; however the private beta alone has made it our fastest-growing pre-seed investment ever by revenues.

2. Código is building a blockchain developer platform that enables web2 developers to build dapps in a few lines of code prompts. With Código’s code generation SDK, developers can create boilerplate smart contract source code, client libraries, and documentation to launch full-service dapps on Solana in minutes. Código’s founder is a former French marine and Bain consultant who spent the past five years founding and exiting an AI developer tools business. He is working with several of our portfolio companies to create templates to launch skeleton DePIN projects in seconds. The costs to launch a new DePIN has fallen an order of magnitude since EV3 was founded; we believe Código will drive the next order-of-magnitude improvement.

3. Unofficial is building web3-native social media products for health-focused communities. Unofficial’s founder led key engineering initiatives at Spotify and Peloton before launching the first viral e-commerce app on Farcaster. Digital health is benefiting from long-term tailwinds in user demographics - younger generations increasingly weaving health & fitness into their social fabric (see: Strava/Flo/Noom/Headspace serving millions of active users) - hardware advancements - with the rise of inexpensive mass-market health monitoring devices (see: Oura rings, Fitbit wristbands, and incumbents like Apple/Samsung making a big bet on smart rings) - and lastly in data interoperability - with web3 social media networks like Farcaster and Lens enabling communities that span across platforms, countries, and languages. Unofficial is building products at the intersection of these trends to drive community-centric digital health experiences.

4. Free Market (FM) is building crypto-native developer automation tools that enable developers to integrate crypto data in a low-code/no-code fashion (web3 Zapier). DePIN middleware has historically been dominated by three use cases: oracles ($LINK), RPCs ($POKT), and indexing ($GRT). We believe two products - agent-based security audits and low/no-code integrations - will lead the next wave of growth in onchain developer services. FM’s co-founders spent the last decade integrating financial data at scale at Visa and Tokensoft, launched FM together in 2023, and are generating seven-figures of net ARR today.

5. Qiro is building an Asia-based institutional private credit protocol that connects onchain capital with high-yielding emerging market borrowers. While Qiro is our furthest foray outside of DePIN, we believe the founding team is well-worth making the exception for. They have built unique regional and technical expertise to navigate local licensing requirements in Asia, and - more importantly - we see a level of hustle, ambition, and long-term partnership focus within them that rivals our own. We are mobilizing our networks in the financial services industry to support the company’s adoption by institutional lenders.

We deployed to double-down on three existing portfolio companies during the quarter. We more than tripled the Fund’s ownership in these companies - from to on a blended average basis - at a point in time when each of them is hitting a steep growth inflection. Expect us to keep proactively doubling-down immediately upon building independent conviction in a project’s momentum, rather than waiting for the next round to materialize at (more often than not) market-clearing terms. With the Fund now halfway through its investment period, we will have more opportunities like this to take advantage of information asymmetry within the portfolio.

1. Daylight is a decentralized energy network that accelerates the buildout of distributed energy resources. Daylight rewards its community for connecting energy meters, batteries, solar panels and other smart devices to the electric grid in order to enable programmable virtual power plants and other software/AI-based energy applications.

We made a non-core investment into Daylight in Q2’23, partially because we felt the energy industry might not be ready for crypto, but primarily because the thesis was too far outside our circle of competence. We spent the past year learning, and in Q1’24 it became obvious the AI chip-shortage will eventually spill over into energy shortages. We spoke to (government-backed) grid operators, (venture-backed) VPP startups, and (owner-operated) installers and realized that: 1) the world desperately needs more electrification—and more electrification means easier electrification, 2) it’s probably impossible to grow at venture-speed while interfacing directly with grid operators, and 3) networks that require trust to bootstrap value lose out to those that use value to bootstrap trust.

Our research led us to doubling-down on Daylight as the first core energy bet in the Fund. You can read more about our thesis in our Q2’23 memo . For homeowners, Daylight collapses the mental overhead of electrification & subsidizes upgrades with token incentives. For installers, Daylight collapses customer acquisition costs and enables trustless collaboration between installers. For developers, Daylight provides real-time granular energy data that can be used to build an ecosystem of energy apps, starting with VPPs. Since our initial investment, Daylight has integrated dozens of the biggest smart energy device manufacturers, launched a consumer mobile app and contractor platform, and designed an energy monitor with thousands of units in inventory.

Given the nature of the solar/battery industry, revenue and gross profit figures can get big fast even with modest amount of units sold. For example in 2021, Goodleap generated more free cash flow than any other private fintech company on earth by reducing the costs/friction of home electrification by an order of magnitude. By 2025, we believe Daylight can generate the highest onchain revenues in all of DePIN by doing the same.

2. 3DOS is a decentralized manufacturing network that enables on-demand manufacturing via a global network of 3D printers. Designers can upload blueprints (in CAD format) and earn perpetual royalties whenever someone orders a print. Printer-owners can monetize underutilized 3D printers by fulfilling third-party orders. Consumers and businesses can order physical products on-demand while saving on shipping time/costs and reducing carbon footprints.

The 3D printing industry has been on an exponentially-declining cost curve for over a decade. 3DOS’ founder has been there since the beginning, starting 3DPrinterOS in 2013 and growing it into one of the leading printer operating systems with 4m+ parts printed. Today, you can buy a new consumer-grade 3D printer for <$400 and set it up in less than 20 minutes; comparable to many DePIN miners. The existing printer fleet is primarily owned by enterprises (e.g. Microsoft/Google/Bosch) and research institutes (e.g. MIT/Berkeley/Yale/NASA) but sees shockingly low utilization rates below 10%.

3DOS will launch in while seeding all three sides of the network with initial momentum. On the supply-side, the 45k+ printers currently running 3DPrinterOS can join the network in one-click and begin monetizing excess capacity. On the inventory-side, users can order from millions of historical designs from 3DPrinterOS or create new AI-generated designs. On the demand-side, the company is finding early product-market with crypto projects ‘airdropping’ physical merch to their communities, including 3D-printed phone cases for all Solana Saga owners. Outside crypto, 3DOS is driving early demand through integrations with web2 e-commerce platforms to whom they can offer structurally cheaper prints.

E-commerce has grown from 2% to 20% of commerce over the past two decades. Along the way, a handful of platforms emerged to enable the long-tail of emergent digitally-native merchants: Shopify abstracted away the storefront and built a $100B+ business, and Stripe abstracted away the cash register and built a $100B+ business. However no one has cracked the missing third piece of the e-commerce stack: the backroom/factory. 3DOS is the missing piece that will enable merchants to manufacture goods globally on-demand in a few clicks or lines of code.

3. MintStars is a creator content platform that uses crypto rails to serve disenfranchised creators in the adult content industry. Despite the scale of the adult content industry - 5 of the top 15 most-visited websites in the world are dedicated to it - its creators are routinely de-platformed by the legacy financial system and social media incumbents. MintStars gives each creator/fan a crypto wallet and facilitates direct peer-to-peer interactions between them. Using stablecoin rails (vs credit/debit cards) reduces chargebacks and payout times to zero, while using NFT rails (vs centralized content hosting) disincentivizes piracy and unlocks perpetual earnings streams. This strategy allows MintStars to charge a 5-8% platform fee vs 20% for the market leader OnlyFans.

We made a non-core investment into MintStars in Q2’23, partially because we felt it was too far outside DePIN, and primarily because it wasn’t clear that adult content creators would flock to yet another new platform after being rugged again, and again, and again. Since then, MintStars has invalidated the latter concern by putting up 10x revenue growth in the past quarter and acquiring 1.5k+ creators organically. Meanwhile, other startups building in the space have either pivoted away from adult content or towards AI-generated content. We believe the bulk of industry profits will be captured by the long-tail of human creators, especially since younger generations are treating pornography as a pseudo-extension of dating (akin to peer-to-peer interactions) vs older generations who saw it as a form of entertainment (akin to one-to-many interactions). MintStars is best-positioned to capitalize on this trend.

1. Zeppelin is a decentralized edge compute & data intelligence network that uses high-value locations to deploy compute/sensors for crypto mining, AI inferencing and other advanced use cases. Zeppelin was founded in 2022 by the former CEO and CBO of Linksys, the leading manufacturer of residential WiFi routers in the US. Over the past year, the company struck a partnership with the country’s biggest billboard operator to deploy on several thousand locations across the US and subsequently became the largest miners of several DePINs, including our portfolio company XNET. Zeppelin plans to launch a general-purpose data intelligence network in 2024 focused on enabling high-value, low-latency use cases on top of its edge infrastructure.

2. Natix is a decentralized mapping network that uses smartphones and other edge sensor devices to enable the long-tail of mapping of use cases. We believe mapping is one of the most important - and valuable - use cases of permissionless global coordination. Over the past year Natix has built a community of 85k+ active drivers across 170+ countries. While most investors focus on the Natix vs Hivemapper comparison, we think it’s a false dichotomy and own both assets. Hivemapper uses dedicated hardware - dashcams - to produce high-fidelity map data for ADAS, autonomous vehicles and other use cases where the ultimate bottleneck is bandwidth. Natix uses commodity hardware - smartphones - to produce low-fidelity events data for the long tail of use cases where the bottleneck is edge compute. As the demand-side becomes clearer for both networks, investors will see the nuance and bid both networks based on their traction and respective end-markets. We note that Hivemapper’s current token valuation is 30x higher than our entry price into Natix, while its community is only 30% bigger. Natix plans to launch its native token in the next 60 days.

3. Repl.Fi is a DePIN repledging protocol that connects tokenholders (lenders) and miners (borrowers) in stake-based DePIN networks. Miners can borrow tokens from the protocol to fulfill larger jobs, and tokenholders can lend tokens to the protocol to earn incremental yield. The protocol manages leverage based on the underlying slashing criteria for each miner, minimizing credit risk while offering 2x higher yields than traditional (unlevered) liquid staking. The Repl.Fi team spun out of Protocol Labs in 2023, launched its flagship $pFIL repledging product in January, and quickly grewn to $40m TVL (vs $100m for stFIL and $400m for GLIF, their primary competitors). Repl’s long-term vision is to build a unifying node trust layer that uses leveraged restaking of assets like FIL, BTC, and SOL to lend economic security to newer DePINs.

Liquid Markets

DePIN’s top quarterly performers in the liquid markets were compute networks catalyzed by new product launches like Arweave (+300%), ATOR (+330%), and Nosana (+520%). The quarter’s worst performers were networks with concentrated insider ownership/unlocks like Hivemapper (+25%), Helium (-10%) and WiFi Map (-25%).

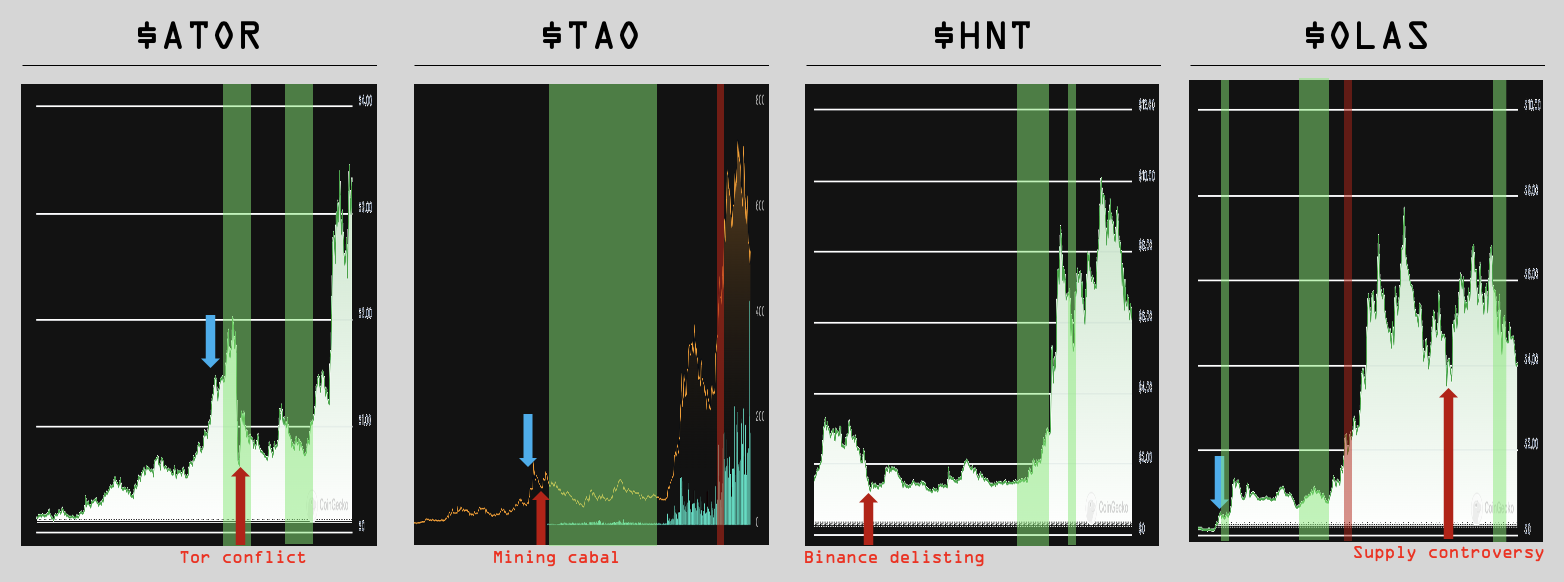

The latter is not surprising. As liquid tokens valuations rise, crypto VCs take advantage of dislocations in portfolios by selling liquids to redeploy into private deals, just as we did in Q1. Extrapolating, we believe 2024 will be characterized by a barbell-shaped return dispersion: networks backed by top VCs will outperform because holders can raise new funds in lieu of selling existing positions, and networks backed by retail (memecoins) will outperform because holders have nothing better to re-deploy into i.e. no access to private deals. Networks stuck in the middle - those backed by VCs with short time horizons - will deliver the worst returns. There is a subset of VCs active today who will invest in nearly anything - at nearly any valuation - so long as tokens unlock within 3-6 months and they can invest in the next shiny thing. This is literally their underwriting criteria. We do everything we can to avoid being on cap tables with these folks. In general, our mental model for the crypto markets in 2024 is as follows: strong VCs will double-down on top-performing private companies in their portfolio in Q1/Q2; by late Q2/Q3 the best projects will have raised through-the-cycle capital (pre-seed will be relatively immune). Weak VCs will sell liquid tokens to re-deploy into the long tail of overvalued private rounds; by the time these tokens launch in Q3/Q4, the capital will have disappeared into the coffers of centralized exchanges and market makers. Finally, an outsized number of the top-performing tokens will be those that used fair launches or token taxes to avoid concentrated insider ownership. In so-called ‘fair launches’, projects forego venture funding to instead finance protocol development with a 5-10% tax on all onchain trades. Successful fair launches have created outcomes comparable to venture capital, raising several million dollars based on trading taxes alone over a few weeks. Taxes are usually lowered or removed once teams raise sufficient capital. The Fund’s biggest liquid winner in Q1 was the fair-launched token $ATOR. ATOR a decentralized private computing network that adds crypto-incentives to the core onion routing encryption technology developed by Tor over the past two decades—roughly analogous to BitTorrent and $BTT. Tor is a decentralized file-sharing network that leverages concentric encryption, also known as onion routing, to encrypt internet traffic in a peer-to-peer way. ATOR began issuing token incentives to Tor node operators who set an Ethereum address as their node header in February 2023, and by October 2023 represented more than a quarter of the entire Tor network. Like many of our best-performing liquid token investments, we developed conviction in ATOR after seeing the network face an existential crisis and bounce back stronger. In November, To r banned all ATOR nodes because the Tor foundation’s leaders - unelected volunteers - held a fundamental stance against crypto incentives. The next day, on a Saturday morning, ATOR’s founding team called us to explain the situation; by Sunday night, they had hired legal counsel to assess their options; and by Monday afternoon, they had announced plans to fork Tor and launch a new privacy-centric decentralized computing network. We doubled-down on Tuesday—$ATOR is up >300% since. Blue arrows below represent our learning about a network, red arrows represent market controversy, green/red bars represent EV3 purchases/sales.

As early-stage private markets heat up, we are finding some of our highest-conviction ideas in the early-stage onchain markets which are relatively untouched by institutional capital. We made two investments into public raises of projects that we passed on in private rounds : Glow, a decentralized network of micro-grid solar plants, and , a decentralized sensor network for drone detection. Glow designed a novel crypto-economic mechanism that guarantees the additionality of solar farms and enables solar operators to generate carbon credits rather than renewable energy credits (the former is a roughly 5x bigger opportunity globally). Glow has onboarded seven solar farms to date and is currently generating ~$1m in onchain ARR, making it a top-10 DePIN by revenues. At its current 25x multiple, Glow is the cheapest DePIN exposure out there on the basis of multiples of circulating market cap. As Glow moves from its current guarded launch phase to a full public launch this summer, we believe it has a chance to become a consensus way to express a ‘renewables/climate’ thesis onchain, similar to how compute tokens have become the consensus expression of the ‘AI picks-&-shovels’ thesis. A re-rating to Helium/Filecoin multiples would drive 10x+ returns from here, re-rating to Render/Chainlink multiples would drive 100x+ returns. Given our investments in the public tokens of these networks, a natural question is why we are not investing in the private rounds. The answer is simple: the terms are often better, either on valuation, liquidity or both. In Glow’s case - while we admire the creativity of its crypto-economic design - we do not believe that an additionality argument based on onchain economic security will convince web2 institutions to buy Glow carbon credits. We do think Glow will be able to sell its voluntary carbon credits to web3 native buyers like protocols and exchanges, but have doubts about the size of this opportunity. If it’s not clear that a market is big enough to support a decade of high-growth compounding, we prefer to own liquid tokens outright with no lockups. The other early-stage liquid investment we made this quarter is OTACON, an AI agent-powered smart contract auditing and bug bounty network. As mentioned above, we believe security audits will drive the next wave of growth in onchain developer services. In Q1’24 OTACON launched an automated smart contract vulnerability scanning tool and a stake-based bug bounty marketplace. The network was fair-launched by an anonymous team and is currently valued at a $2.5m FDV. While $OTACON is further out on the risk curve than our typical investment, we think it has the potential to drive correspondingly asymmetric returns.

We built positions in five large-cap tokens during the quarter, two core DePINs, $HONEY and $FIL, and three DePIN-adjacents, $JITO, $NEAR and $IMX. Hivemapper ($HONEY) is a decentralized mapping community that has mapped >17% of the world’s roads in <17 months with consumer-grade dashcams. Filecoin ($FIL) is a decentralized storage and compute network with nearly 2 exabytes of stored data and likely the largest global DePIN community on earth. To learn more about these networks please check out our State of DePIN 2023 report, or our podcast where we recently hosted Hivemapper founder Ariel Seidman and former Protocol Labs ecosystem lead Jonathan Victor.

We made three investments into L1s or correlated exposures that we believe will see significant DePIN activity over time that the market is not yet pricing in. Near ($NEAR) recently reinstated their founder Illia Polosukhin as CEO of the Near Foundation and has been executing at an impressive pace since, including courting a number of stealth DePIN projects. Jito ($JITO) runs staking and MEV infrastructure for Solana. DePINs on Solana are able to put core network activities onchain, rather than simply settling payments onchain on Ethereum, which means it is likely where DePIN MEV will emerge first, with Jito playing a critical role. Like many of our best liquid investments, we doubled-down on Jito after seeing the network manage a mempool controversy and come out with a stronger position in the community on the other side. Immutable ($IMX) is the leading public blockchain for gaming developers. We believe crypto gaming and DePIN will converge as game developers strive for economic sustainability and as DePIN networks strive to gamify an increasingly-broad set of real-world activities.

As always, we are eternally grateful for your support and encouragement. In Q2’24 we will be traveling to Asia and Latin America to meet entrepreneurs building DePIN on-the-ground at the forefront of emerging markets. We appreciate introductions to any founders, investors or operators you think highly of. We will also be hosting our first AGM on May 16th in New York City, and hope to see many of you there. Please let us know if you have not yet received the invite, originally sent in March, and would like to attend.

Your partners,

Sal & Mahesh